With a constantly-increasing list of financial firms in the Houston area, it’s no wonder that many consumers struggle to pick the right one. Between Financial Advisors, Financial Planners, Investment Advisors, Broker-Dealers, and dually-registered firms, there are a plethora of choices for wealth management professionals that each has its own fees, investment philosophies, pros, and cons.

What’s the difference between the types of advisors?

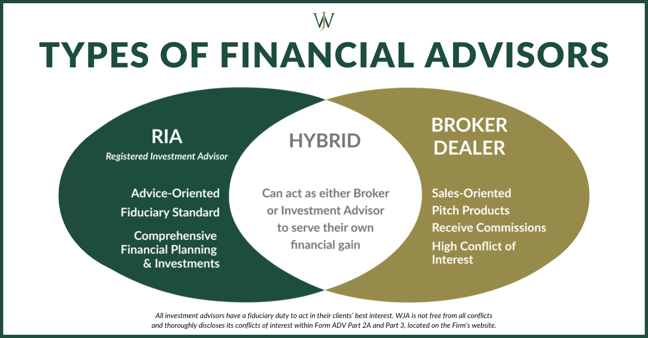

What is a Broker-Dealer?

According to Kitces, “broker-dealers [are] a fundamentally sales-oriented transactional business, as the job of broker-dealers, and the stockbrokers they employ, is literally to facilitate the purchase and sale of investments (for themselves or their customers), for which they are paid a commission or mark-up for effecting the transaction. Accordingly, broker-dealers are [historically] subjected to a “suitability” standard – that in the process of selling securities to and on behalf of their customers, they only make recommendations that are not unsuitable for that customer.”

In my opinion, brokers-dealers are like the muddy waters created by the Reg BI rulings. They don’t want you to know that you’re meeting with someone in a product-sales role who can get paid in non-transparent ways including commissions, kickbacks from mutual funds, or other means.

What’s a Registered Investment Advisor (RIA)?

Registered Investment Advisors, like those at Willis Johnson and Associates, are held to the highest fiduciary standards in the industry. A fiduciary standard is one involving trust, or, is one to be held or given in trust. RIAs have fiduciary obligations to their clients, which means they have a fundamental duty to always and only provide investment advice that is in the best interests of their clients.

Additionally, under Section 206 of the Investment Advisers Act of 1940, RIAs have a stringent requirement not to engage in “any device, scheme, or artifice to defraud any client or prospective client.” The case of SEC vs Capital Gains Research Bureau proved the need for RIAs to perform fully-fledged fiduciary duties for their clients given the relationship of “trust and confidence” that exists between a client and his/her advisor.

In short, we hold the trust and confidence of our clients and prospective clients to the highest standards and only work in their best interest.

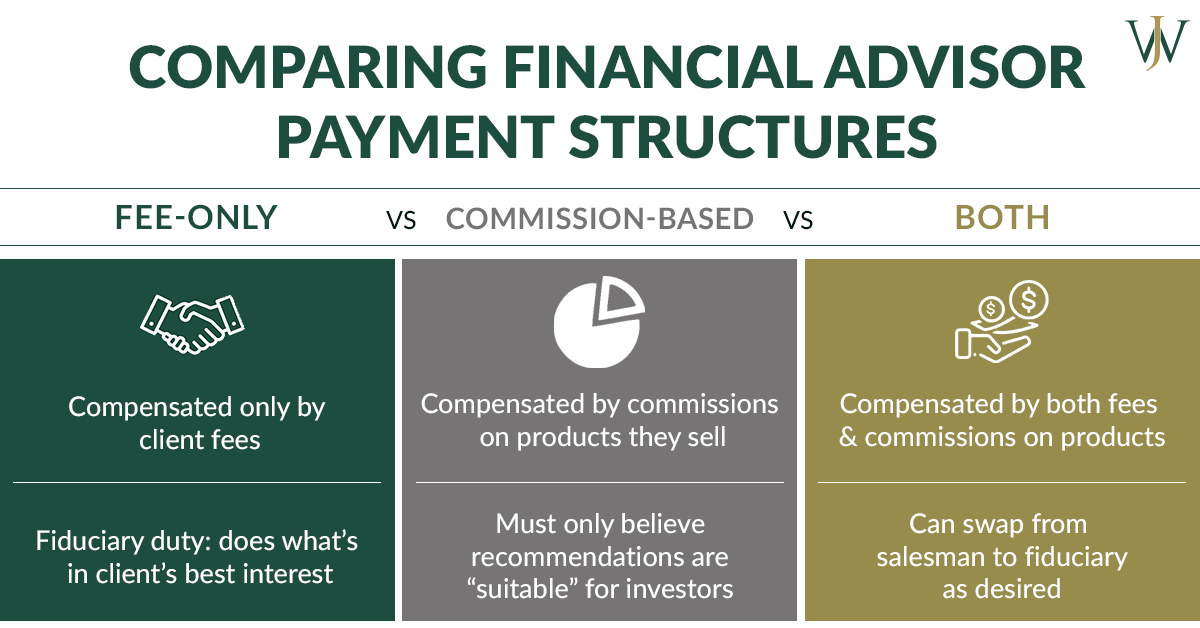

As an RIA, we get paid the same way no matter what our clients invest in. We make an effort to be extremely transparent, which is why we put a fee calculator on our website and walk our clients through their investments and our strategies multiple times a year.

To summarize: brokers are set up to sell (or buy) securities. Registered Investment Advisors were initially set up to give fiduciary advice to the consumer.

Brokers = sales

Registered Investment Advisors = advice

What if my advisor is dually-registered or is a hybrid advisor?

There are also dually-registered individuals or hybrids that are registered as both Broker and Investment Advisors. To me, this is even more concerning for consumers! These professionals can put down one hat and pick up the other hat at any point in time acting as either a Broker or Investment Advisor from minute to minute to serve their own financial gain.

SEC Rules Make It Difficult to Know Who's a Fiduciary Financial Advisor

The SEC, the organization in charge of regulating the financial services industry, recently implemented a set of rules and interpretations regarding the financial advice given by brokers. This set of rules is referred to as Regulation Best Interest, or Reg BI, and was intended to make it simpler for consumers to know if the person advising them is working in their best interest.

Since the release of this rule in 2019, XYPN, run by well-known Financial Advisor blogger Michael Kitces, seven states, and the District of Columbia have each filed lawsuits against the SEC over these Reg BI rules. The rules are complicated and nuanced, but you can read a summary published on Barron’s by the Investment & Wealth Institute here.

The 4 major obligations all financial professionals must follow to comply with the SEC are:

-

- Brokers are required to act in the best interest of the customer when recommending investment products or strategies; when making account changes, they must also do so without placing their firm’s interests ahead of the customer’s

- Brokers must provide full disclosures of both their recommended products as well as their status as a broker-dealer, fees, scope of services, and any conflicts of interest

- Brokers are required to exercise reasonable care when making recommendations of products which only requires a “reasonable basis to believe” the recommendation is in their customer’s best interest

- Conflicts of interest must be, at a minimum, disclosed or mitigated if related to the recommendation a broker makes to their client; however, the ruling doesn’t require that these conflicts of interest are eliminated

While these rules are required to be followed in order to comply with the SEC, the flexibility in them allows for different ideological interpretations among different types of advisors.

What is the Real-World Impact of the SEC’s Regulation Best Interest (Reg BI) Rulings?

In our opinion, the problem with Reg BI is that it allows Brokers to more easily provide advice to consumers without being held to the same standard of care as Registered Investment Advisors, causing more confusion for the consumer.

Through the Dodd-Frank Wall Street Reform and the Consumer Protection Act of 2010, Congress stated that fiduciary advisors must “provide personalized investment advice about securities to a retail customer… the standard of conduct for such broker or dealer, with respect to such customer, shall be the same as the standard of conduct applicable to an investment adviser”— meaning that, if brokers are able to provide ‘advice,’ then they must also be Fiduciaries.

In reality, the SEC (through Reg BI) has now allowed brokers to provide one-time advice that is “solely incidental” and is “in connection with and reasonably related to” the sale of products. The area of ‘advice’ is clearly laid out by Congress to be under the domain of Registered Investment Advisors. According to the Dodd-Frank Act, if Brokers provide advice, then they should be held to the same standard as RIAs—but they aren’t!

Another thing to note, and Kitces points out succinctly, is that “…the SEC effectively positions RIAs in Regulation Best Interest as [those who provide] ongoing advice and investment management services, implying that more ‘transactional’ advice is the domain of broker-dealers. In fact, in the original version of Regulation Best Interest, the SEC repeatedly referred to broker-dealers as the deliverers of “episodic” advice.”

How Can I Tell If My Financial Advisor is a Fiduciary?

For client-facing roles working for Registered Investment Advisors the most common title is “Financial Advisor.” Guess what the most commonly used title for Brokers is? You guessed it—it’s also “Financial Advisor.”

How is the consumer to know whether they are working with someone in a sales-oriented role or an advisory role? They don’t. The SEC allows the title of “Financial Advisor” for dual-registrants as long as they disclose that they may act in multiple different capacities, either as an advice-giver in the client’s best interest, or as a salesman. I can tell you from personal experience that very few people read the disclosures given to them and, almost no one who does read them understands them.

How To Find Out if Your “Advisor” is a Broker &

What To Do Next

- To determine if your advisor is an RIA or a broker, look them up on the government-run website: brokercheck.finra.org. If they are listed as a Brokerage Firm or a Broker, the ‘advisors’ that work there can get paid in non-transparent ways by recommending investment products.

- If there are disclosures on brokercheck.finra.org, make sure to read them. These disclosures can be anything from customer disputes, criminal charges and convictions, or regulator disciplinary action. Both the firm as well as the individual can have disclosures.

- If they are a broker, ask that they provide a list of all the ways they get paid from working with you in writing.

- When working with a Broker, they may offer you something that sounds a lot like advice. Be warned that it could be “solely incidental” and “in connection with and reasonably related to” sale of products. If they provide advice, ask them in writing if they are acting in a fiduciary capacity when they are providing you that advice.

Due to poor regulation, it’s difficult for consumers to know if they are working with a fiduciary or not; however, at the end of the day, most people in the financial services industry (including the majority of Brokers) are in it to help those they serve.

At Willis Johnson and Associates, we take pride in acting in our client’s best interests — not just because of our fiduciary obligation, but because we think it’s the right thing to do. We believe in educating our clients on the questions they need to be asking, the answers to those questions, and giving them a road map to a successful financial future.

All investment advisers have a fiduciary duty to act in their clients’ best interests. Willis Johnson & Associates is not free from all conflicts and thoroughly discloses its conflicts of interest within Form ADV Part 2A and Part 3, located on the firm's website.