Corporate professionals and executives have the unique opportunity to boost their non-retirement savings through an Employee Stock Purchase Plan (ESPP). Designed to encourage employees to “buy-in” to the success of their employers, ESPPs offer the ability to purchase company stock at a discount to fair market value.

How an Employee Stock Purchase Plan (ESPP) Works

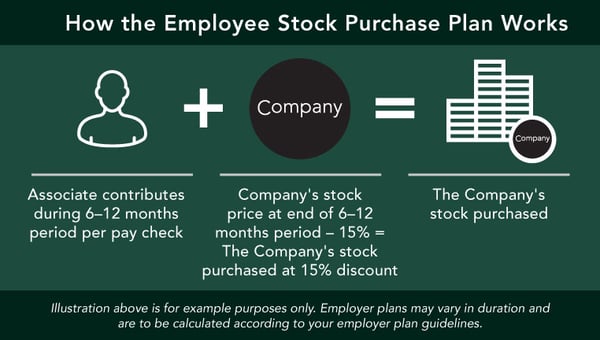

Contributions to an ESPP are deducted directly from the employee’s paycheck after enrolling in the plan. At the end of the plan year, shares of the company stock are then purchased using the employee’s cumulative contributions. A specific share price valuation date is predetermined and some plans select from multiple valuation dates, ultimately purchasing shares on the lowest-cost day. In addition to receiving the lesser of two or more valuation prices, plans also offer an employee discount of up to 15% from the share purchase price.

The Benefit of an Employee Stock Purchase Plan

The ability to purchase stock at the lesser of two valuation dates and at a guaranteed discount is a huge benefit.

Assuming a $9,000 contribution to the ESPP.

Had this employee simply purchased $9,000 of company stock on the last day of the plan year they would only receive 125 shares. By participating in the ESPP however, this employee ends the year with 162 shares of company stock. This equates to a total discount of more than 30% per share!

Let’s say the stock price decreased over the course of the plan year, ending the year at $59 per share. Again, stock is purchased at the lower of the two valuation dates, in this scenario $59. After the 15% discount the employee would receive stock at just $50.15 per share for a total of 179 shares. Regardless of which direction the stock price moves, shares are purchased at a lower valuation.

Considerations for Enrolling in an Employee Stock Purchase Plan

Before enrolling in an ESPP it’s important to understand the tax implications involved before the stock arrives in your brokerage account. There are two types of ESPPs: qualified and non-qualified. Most U.S. employers who offer an ESPP have followed the IRS code and established their plan to meet the qualified status requirements.

Assuming the plan is qualified, there is a further distinction made when the stock is actually sold depending on the length of time the employee held the purchased shares. Shares held at least two years from the offer date and one year from the purchase date will receive preferential capital gains tax treatment. Shares held less than two years from the offer date or less than one year from the purchase date will be taxed at ordinary income rates when sold. No matter how long you hold the stock, the original 15% per-share-discount will be taxed at ordinary income rates.

Continuously participating in an ESPP can generate significant value over time by amplifying the non-retirement savings the employee was already doing. Along the way, it’s important to consider the over-concentration risk of owning an ever-growing amount of stock in a company you also work for. This risk can be mitigated by routinely selling stock each year as new stock is purchased. This laddered approach preserves the tax benefits of holding each lot for one year while also allowing the employee to diversify their holdings to broad-market investments.