Are you meeting all of the specific requirements to reap all the benefits when making a Qualified Charitable Distribution? Make sure you are not leaving money on the table.

What is a Qualified Charitable Distribution?

If you are over the age of 70 ½ and charitably inclined, you can send a portion of your IRA’s Required Minimum Distribution directly to a charity and thereby lower your adjusted gross income and potentially decrease phaseouts and Medicare premiums.

The IRS passed the PATH Act of 2015 to permanently allow qualified charitable distributions (QCDs) every year. Previously, Qualified Charitable Distributions had been reinstated annually for the preceding year, which made the use of QCDs for tax planning a little more difficult. The QCD allows an individual who has reached the age of 70 ½ to send a portion of their RMD from an IRA directly to the charity of their choice.

What is the Maximum Amount for Qualified Charitable Distributions?

The limit on the amount that one can send to charity is $100,000 and the distribution must be made from an IRA, not a 401(k). The $100,000 limit is per individual, so a married couple may each send up to $100,000 from their respective IRA’s RMDs to a charity.

There are several reasons why it may be important for an individual or married couple, who is already charitably inclined, to send their RMD directly to charity. First, it decreases your Adjusted Gross Income (AGI). Instead of including your entire RMD in your AGI and then making a donation to charity for a deduction, you can send the amount you would have donated directly to a charity and it will not be included in your AGI. You still end up giving the same amount to charity while decreasing your AGI.

Second, as your AGI increases, you begin to have an increase of phaseouts on deductions and exemptions as well as an increase in Medicare premiums, which then increases your taxable income. By sending a portion of your RMD directly to a charity, you can attempt to avoid some of the phaseouts that occur at a higher AGI.

Consider the following hypotheticals:

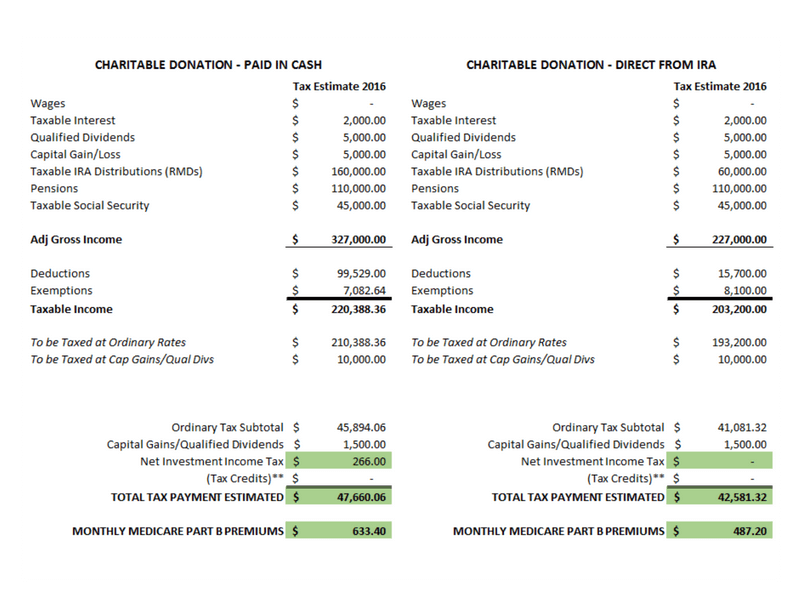

A married couple in their late 70's wishes to make a large donation to their favorite charity. Their current AGI, including their RMDs of $160,000, is $327,000. They make a donation of $100,000 and deduct the amount on Schedule A of their tax return. Their total estimated Federal Income tax payment is $47,660. Since their AGI is over the threshold for phaseouts, they will lose part of their deductions and their exemptions. They will also have higher monthly Medicare premiums and will be required to pay the Net Investment Income Tax.

If the same couple sends $100,000 of their RMDs directly to charity, their current AGI will decrease to $227,000. They will not list a charitable deduction on their Schedule A. Their total estimated Federal Income tax payment will be $42,581. Not only are they paying less in Federal Income taxes and Net Investment Income tax, but they will be paying less in Medicare premiums as well.

See comparison below:

If you do decide to make a QCD, it is key to remember to have your IRA’s custodian make the check payable to the charity and not to you as the owner. If the check is made out to you, there is no way to correct this mistake and the money will be deemed as part of your adjusted gross income. Additionally, the charity must be a public charity, not a private foundation nor a donor-advised fund. It is also important to note that a QCD can only by made from a Traditional IRA or an Inherited IRA where a beneficiary is over 70 1/2 years of age. You cannot make a QCD from a Simple IRA, SEP IRA, or 401(k), as these are considered employer-sponsored plans and are excluded from the rule.

Taking advantage of the newly permanent QCD law is a tax-efficient way to keep your income lower and pay fewer taxes while still being able to give to the charity of your choice.