Occasionally, we all regret an investment decision. We purchase a security thinking it is going to be a high performer, but it sinks in value instead. We hold on to the security, thinking that surely the value will rebound at some point. But the rebound never happens.

Is there any way to make this situation less painful?

Yes — we can “harvest” those losses against our income, using the loss to bring us valuable tax savings.

How Can Tax Loss Harvesting Offset Investment Losses

When stock is sold from a taxable account, the investor incurs either a gain or a loss, based on whether the value has increased or decreased from the purchase price. If you’ve held the stock for less than a year, the nature of the gain or loss is short-term and is taxed at ordinary income tax rates. If you’ve held the stock for more than a year, the gain is long-term and is taxed at capital gains rates, which is oftentimes more favorable.

Tax loss harvesting requires the investor to know which positions in his/her portfolio are in a gain or loss position. You can use your investment losses to lower your tax liability if you are savvy about which stock you sell and when you decide to sell it.

3 Common Mistakes We See Investors Make

How Does Tax Loss Harvesting Work

Let’s look at an example. An investor, who is in the 35% ordinary income tax bracket, has the following stocks included in his portfolio:

| Stock A (Short-Term) |

Stock B (Long-Term) |

Stock C (Long-Term) |

|

|

Number of Shares Purchased |

1,000 | 1,000 | 500 |

|

Price Per Share When Purchased |

$70 | $90 | $30 |

|

Price Per Share At Current Value |

$100 | $50 | $40 |

|

Result |

$30,000 |

$40,000 |

$5,000 |

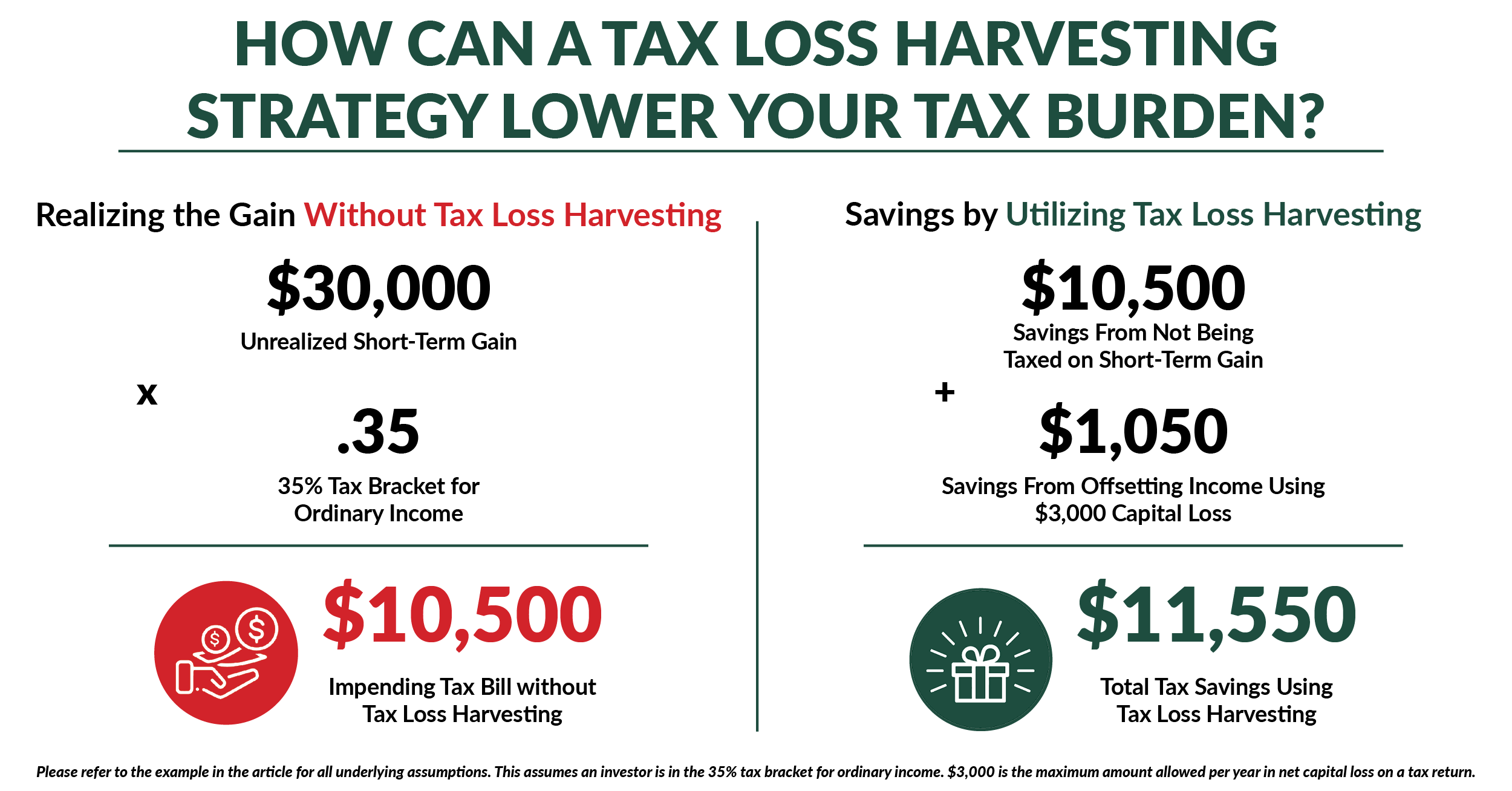

Our investor wants to sell Stock A to capitalize on its performance. However, the $30,000 short-term gain will be taxed at the investor's ordinary income tax rate, which is 35% in our example. This tax bite is $10,500, almost ⅓ of the gain!

What if the investor decides to also sell Stock B and C during the same year to harvest these losses to offset the gain?

The IRS requires investors to report gains and losses in the following manner on their tax returns:

- Net short-term losses against short-term gains;

- Net long-term losses against long-term gains;

- If there are any excess gains/losses after steps 1 and 2, net excess short-term gains or losses against excess long-term gains or losses.

Putting this rule into practice, the investor would net gains and losses as:

| Short-term gain from Stock A: | $30,000 |

| Long-term gain (loss) from the sales of both Stock B and C | |

| Stock B loss | ($40,000) |

| Stock C gain | $5,000 |

| Net long-term loss | ($35,000) |

| Net long-term loss against short-term gain: | |

| Short-term gain | $30,000 |

| Long-term loss | $35,000 |

| Net loss | ($ 5,000) |

Now, be aware that the IRS will only allow $3,000 per year in net capital loss. Consequently, our investor will be able to include $3,000 loss on his current tax return to offset his other ordinary income. The remaining $2,000 loss will carry forward to his next year’s tax return.

What is the tax result of an investor “harvesting” his losses against his short-term gain in this example?

Now, recall that if the investor had not sold Stocks B and C, his tax bill on the gain would have been $10,500. Not only does the investor eliminate his short-term gain, but he is also able to offset other ordinary income (such as salaries and interest) by the $3,000 excess capital loss. This results in additional tax savings of $1,050 ($3,000 x 35% tax rate of the investor in this example). The total tax savings in our example is $11,550!

If an investor has already realized gains from previous sales during the year, as this example illustrates, tax savings are made available by taking these two loss-harvesting actions:

- Before the end of each year, investors should take a look at the unrealized gains and losses of their holdings.

- Investors should determine the tax benefits of selling stocks in loss positions to offset the realized gains and up to $3,000 of ordinary income.

IRS Rules That Affect Tax Loss Harvesting

While there are significant tax benefits to harvesting losses on investments, it’s important to understand the IRS’s wash sale rule to ensure that your loss harvesting is allowed.

The IRS “wash sale” rule disallows the recognition of a capital loss on the sale of a security if “substantially identical” securities are purchased 30 days before or 30 days after the date the loss-generating security is sold.

A security is “substantially identical” if it is:

- The same stock as the stock that was sold.

- A different class of stock, but issued by the same corporation.

- An ETF tracking the same index, even if offered by different investment firms.

A loss could be excluded, in whole or part, if the wash rules are not followed. (Note that inadvertent violation of the wash sale rules can occur if a dividend reimbursement election is in place on a particular security and a reinvestment takes place within 30 days of the loss transaction.)

When Should You Do Tax Loss Harvesting?

Tax loss harvesting remains a relevant strategy, particularly for investors in higher tax brackets, those holding concentrated stock positions, or those who realize gains from equity compensation or portfolio rebalancing. Especially when the stock markets are volatile, there can be a tremendous opportunity for investors to rebalance their portfolio and realize losses for future use and benefit.

For example, in April 2025, when President Trump announced tariffs, the S&P 500 dropped 12% in a single day. These sudden losses, while scary for most investors, created a tax loss harvesting opportunity. Let's consider another example where you have vested company share grants and may be reluctant to sell those shares at the prevailing market price. If you sold some shares this year, you could realize losses to offset realized gains from future sales. With a well-guided strategy regarding the cost of stock holdings and a clear investment outlook, you can begin to execute a plan for rebalancing your portfolio and deconcentrating from stock holdings.

There are many reasons and potential applications for investors to employ tax loss harvesting. You should seek the counsel of your tax advisor and financial advisor when implementing a loss harvest to maximize the benefits of this strategy. The wealth managers and in-house tax team at Willis Johnson & Associates implement tax-loss harvesting strategies for our clients to proactively find tax-efficient solutions. If you have any questions, please don't hesitate to contact a member of the Willis Johnson & Associates team for more information.