A National Association of Plan Advisors survey found that approximately 55% of Americans with incomes over $100,000 work with Wealth Managers. As more people look to work with financial advisors, the financial industry has grown significantly in recent years. So why do people choose to hire a wealth advisor? The reason is simple: Americans want to ensure they make the most of their finances and set themselves up to achieve their financial goals.

However, the financial services landscape is competitive, complex, and can be confusing. With so many financial advisory options for consumers to choose from, it can be challenging to differentiate and evaluate the quality of one advisor from another. This article aims to provide a list of "red flags" that should give pause to anyone looking to hire or assessing the quality of their current, Wealth Manager or Financial Advisor.

What to Avoid When Hiring a Financial Advisor:

- Lack of Transparency Around Compensation & Conflicts of Interest

- Only Focuses on Insurance or Annuity Solutions

- Recurring Promotion and Usage of High-Commission Investment Products

- They Don’t Communicate Proactively

- No Focus on Estate or Trust Planning

- No Specialization

- Short-Sighted Investment Strategy

- No Designations

- Tarnished BrokerCheck Record

Red Flag #1: Lack of Transparency Around Compensation & Conflicts of Interest

When you start working with a financial professional, one of the first steps is giving them a look behind the curtain into the various financial details of your life. Taking this first step requires openness and honesty on your part that you likely expect to be reciprocated, right?

Because of how certain firms are set up, some conflicts of interest may result in less transparency from your advisor. When considering an advisor or firm you want to work with, taking a look at what type of firm they are will provide necessary insight into their approach off the bat.

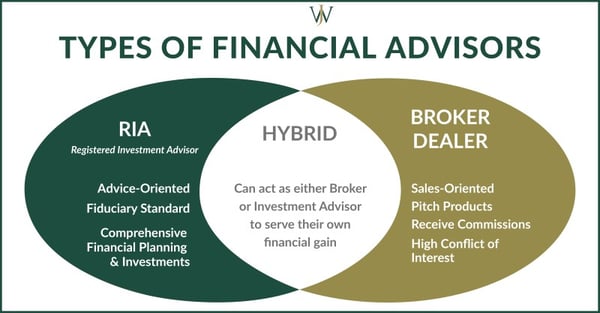

- Broker-Dealer Firms: According to Kitces, “The job of broker-dealers and the stockbrokers they employ, is literally to facilitate the purchase and sale of investments (for themselves or their customers), for which they are paid a commission or mark-up for effecting the transaction. Historically, broker-dealers are subjected to a “suitability” standard, which means that in the process of selling securities to and on behalf of their customers, they only make recommendations that are not unsuitable for that customer.”

- Registered Investment Advisors (RIAs): Advisors and firms with a fiduciary obligation to their clients which means they’re always giving advice in your best interest.

- Hybrids: These firms may act as fiduciaries some of the time, but can also pitch certain investment or insurance products that are suitable, even if they’re not the best solution for you. We refer to these as hybrid advisors because they can wear the hats of either an RIA or a Broker-Dealer firm.

While it’s fair to say most financial professionals want what’s best for their clients, often, this key nuance of how an advisor is paid for the advice they provide gets missed in initial conversations. When entering the preliminary discussions about what value an advisor can provide, make sure you’re asking critical questions about advisor compensation as well as their approach to financial planning to ensure they’re the right advisor for you.

Red Flag #2: Only Focuses on Insurance or Annuity Solutions

A popular adage says, "if one is a hammer, everything looks like a nail."

Numerous broker-dealer and hybrid companies, with names often ending in "Life" or "Mutual," focus exclusively on selling insurance policies and annuities. Insurance is undoubtedly an important piece of any financial plan, but that is precisely what it should be: a piece of one's financial plan, not the entirety of it. Unfortunately, many insurance agents focus solely on the solutions they provide, not the whole picture. Additionally, many are incentivized to assure their clients and prospects not to look beyond these solutions.

If your goal is ensuring that loved ones are taken care of if your family's breadwinner passes away unexpectedly, insurance products can be a great way to pass assets tax-efficiently. However, as a vehicle for savings and investments, insurance and annuities have significant pitfalls.

Which Types of Insurance & Annuity Solutions to Watch For

Certain types of insurance and annuities like Indexed Universal Life, Variable Annuities, and Variable Life Insurance have performance "tied" to the market. While these products sound great in theory, there are better alternatives.

Often, less expensive or better-performing products are better suited for those looking to benefit from market growth. One option is to invest savings into low-cost ETFs in tax-advantaged accounts like Traditional or Roth IRAs or a 401(k). Traditional and Roth IRAs have a vast selection of investment options. Depending on your company, your 401(k) may have an extensive or minimal selection of funds in which you can invest.

By contrast, many annuity and insurance products don't allow for a customized investment selection and limit you to select groups of high-commission funds. For these reasons, we commonly tell our clients that using insurance products as one's sole means of investment is generally a bad idea. Here’s why:

- Higher Fees - When using insurance products, you pay higher fees for the assets' management and the commissions paid to the broker. Before utilizing any insurance product, ask an insurance broker to quantify the fee's costs in writing and by dollar amount instead of percentages or basis points.

- Insurance policies are less "liquid"- If you need to cover expenses immediately, accessing the policy value can be challenging. If you want to cancel the policy within the first several years of its inception, many insurance products have expensive "surrender" fees. Lastly, withdrawals above the premium you paid are generally taxable.

-

Leaving Company Money on the Table - If you are putting money into an insurance product instead of making 401(k) contributions, you may be missing out on your company's match. Many of the clients we work with at Shell, Chevron, and BP receive a generous company contribution or match to the 401(k) between 2-10%. Missing out on these contributions can add up over time as you are refusing "free" money from your employer by not making contributions to the 401(k) plan.

If you notice your financial advisor only recommends and sells you annuities or life insurance policies, you may want to seek out a second opinion. Particularly if these options were pitched as the only option for you, additional counsel from a fee-only fiduciary who doesn't get paid to sell products could be beneficial.

Red Flag #3: Recurring Promotion and Usage of High-Commission Investment Products

Consumers should also be wary of commission-based products. Does this mean that all commission-based investment options are bad? Of course not. But one should be mindful of the excessive use of products like high-fee Mutual Funds, Unit Investment Trusts (UITs), Fixed income SMAs (in a low-interest rate environment), and Structured Products. Let’s break down the most common ones and what to keep an eye out for.

Mutual Funds

Why would an Advisor recommend the use of Mutual Funds? There are two reasons:- They believe that active asset management will prove fruitful in providing above-market returns (vs. alternatives), or

- They stand to make significant commissions from A or C shares.

What's an A-Share Mutual Fund?

A-shares charge an upfront sales fee removed from your principal. Hypothetically, if you plan to invest $100,000 in a mutual fund with a 3% sales fee, only $97,000 is invested and you pay $3,000 in commission to the broker (in this case, your advisor) off the top. At inception, you're already "down" 3% in the investment. On top of that, there are annual fees and expenses associated with all types of mutual funds (paid to the fund managers and its staff), which further diminishes your "net of fee" performance.

What's a C-Share Mutual Fund?

C-shares carry lower "upfront" costs but either has higher annual sales fees or charge a "backend" load in addition to the yearly expense you pay. These fees still hamper your investment's performance value, but the difference is that they are spread out over time instead of being applied at the time of sale like they are in A-shares.

Unit Investment Trusts (UITs)

Regarding fees, UITs, or Unit Investment Trusts, are another relatively-expensive investment vehicle. UITs are similar to mutual funds in that the securities therein are "hand-selected" by an investment manager. However, the major difference between UITs and mutual funds is that mutual funds are actively managed. The fund manager for a mutual fund trades the underlying investments on an ongoing basis to take advantage of changing market conditions while no one actively trades the funds in a UIT. In a UIT, the fund manager selects the investments and the selection remains unchanged for the duration of the fund's life. For many investors, that's not an ideal scenario. Additionally, UITs also entail high sales charges, generally between 1-5% of the investment upon its sale to the consumer as a significant "one-time fee."

Separately Managed Funds (SMA)

Another "expensive" investment product is a Separately Managed Fund, or "SMA" for short. With an SMA, you own the underlying securities in these funds, and the fund manager buys or sells securities regularly to adjust for changing market conditions. Often, advisors recommend SMAs for investors interested in investing in only stocks or stocks and bonds through a diversified mix of fixed-income and equity securities.

However, in low or rising interest rate environments, you should be especially wary of Fixed Income SMAs. A general rule of thumb is fixed income does poorly when interest rates rise. Because the bond's principal declines in value in low-interest rate environments, fixed-income investments don't often provide significant yields in these periods. We often see similar performance for Fixed Income SMAs. If your advisor recommended a "non-high yield" Fixed Income SMA in the last couple of years, you may benefit from opening up a dialogue with them. Understanding why they recommended the SMA as the best option for you can provide helpful insight into how they manage your portfolio and may push you to seek out a second opinion from a different advisor.

Structured Products

The final product to watch for is a "Structured Product." Structured products are reasonably complex bundles of options or derivatives that have a variety of uses. You can use structured products to minimize market risk, structure them to take advantage of a market pullback or run, or even leverage volatility in an asset class or a specific security. Sounds great, right?

Well, there are two issues we often see with structured products. The first is a lack of liquidity and clarity on the product's value. When looking at your account statement for the value of the product, it's often very difficult to understand, let alone explain.

The second issue we find is that, like the other securities mentioned above, structured products also carry high sales fees, often between 2-6%! These fees mostly go to the broker and should be scrutinized carefully. Additionally, the fees should be disclosed both verbally (ideally, in terms of "dollars and cents" instead of expressed only as a percentage) and in writing. Often, these important fee details are hidden in lengthy disclosure statements which is why asking for clear verbal disclosures from your advisor is essential.

Advisor Tip: Look for Low-Cost ETFs Instead

On average, Exchange Traded funds (ETFs) outperform their actively managed counterparts net of fees. ETFs generally have fees between 0 basis points and 50 basis points (the latter equates to 0.5% of the value of the funds invested in them), whereas Mutual Funds generally have significantly higher investment management fees- generally ranging between 100 basis points and 150 basis points (1% to 1.5%). Then there are up-front or deferred sales charges in addition to the annual management fee on mutual funds which are discussed above.

Red Flag #4: They Don’t Communicate Proactively

Most firms agree that advisors should meet with their clients yearly at a minimum, but the more often, the better. When it comes to our clients, we believe that communication is everything. Circumstances can change quickly in the markets, in tax laws, and in the lives of clients. Whether it's the birth of a grandchild or receiving an inheritance from a parent who's passed away, we think it's essential that advisors meet with their clients on a quarterly or semi-annual (at a minimum) basis.

By meeting regularly, advisors stay current on what's happening in a client's life, but clients also know what's going on with their financial plan. All too often, clients see what's happening in the news about the stock markets or they hear from their colleagues first, but a good advisor reaches out proactively with a plan in mind.

Among the topics we discuss with clients regularly, we often evaluate the following:

- Have there been changes to cash flow recently from a promotion or severance?

- Review the clients' tax projections for the year to ensure tax-efficient uses of their available funds

- Examine significant market movements, the impact on the client's financial situation, and the investment strategy going forward.

- Update beneficiaries and contingencies for trusts and estates as assets accumulate.

- Discuss significant life events such as the sale of a business, retirement, or passing or birth of a family member and their impact on a financial plan.

Not only does proactive communication showcase an advisor's care for their clients, but by meeting regularly and reaching out before circumstances change, advisors can stay abreast of changing scenarios and plan ahead. If your advisor seems to always be reacting to circumstances instead of proactively planning for them, it may be in your best interest to walk away.

Red Flag #5: No Focus on Estate or Trust Planning

Some advisors only focus on managing your investments. But, like insurance, those are only one piece of a financial plan. Many advisors focus so much on the investment arm of a portfolio they fail to impress upon their clients the importance of thinking futuristically to have a trust and estate plan in place. The reason behind this is simple: they already have your assets. Creating a trust or estate plan only results in the advisor having to file more paperwork and spend time managing the same amount of assets.

We're big believers in the value estate planning can add to your financial picture. So often, our clients work hard to accumulate their savings and get the most from their investments for those they care about most. A proper estate plan provides clarity and simplicity to your loved ones when unexpected events arise and is an incredible gift to provide for them. If your advisor has not suggested you create or update your trusts or estate plan, it may signal their prioritization of convenience over the welfare of your loved ones.

Red Flag #6: No Specialization

To better stand out in a sea of advisors, many advisors and their firms choose to focus on serving a specific niche. A few of the most common populations advisors work with are doctors, lawyers, corporate professionals, business owners, wealthy families, and professional athletes.

"A jack of all trades is a master of none."

Ensuring that your financial advisor has experience working with clients with similar professional and personal circumstances is essential. You wouldn't want to go to a cardiologist for an eye injury. Similarly, you want to work with someone with vast knowledge of your unique situation and the considerations that come with it. For example, our firm works with corporate executives and professionals in the energy industry. WJA has become renowned for its expertise in optimizing the corporate benefits of professionals at Shell, Chevron, and BP. We have found a host of complexities associated with these professionals' corporate benefits that impact their financial plans and retirement. As such, we help with pension election considerations, tax-efficient decision-making around retirement or severance packages, understanding how LTIP benefits and stock compensation impact their taxes, and much more. For example, many insider executives with stock compensation accumulate and sell their shares in compliance with the company's trading restrictions, which often impacts their concentration in company stock.

Doctors, lawyers, and wealthy families also have complex financial planning needs with similarly high stakes, hence the importance of specialization. If an advisor ignores or doesn't understand how to optimize your corporate benefits effectively, you could be losing out on anywhere from tens of thousands or, in some cases, millions of dollars at retirement. Compensation and benefit packages are complex, and understanding how to minimize taxes to maximize the value is one of the most significant benefits an advisor can offer.

Red Flag #7: Short-Sighted Investment Strategy

At face value, investment performance may seem like a reasonably straightforward measurement. Most investors look at their investments for the percentage of increase or decline in the total aggregate assets within an investment account. However, a short-sighted investment strategy can have long-term repercussions.

Frequently Executing Short-Term Trades

Frequent short-term trading can have a significant impact on your taxes. Securities you've held less than a year get taxed at higher capital gains rates, which add up quickly over time. Too often, advisors lack conviction and want to prove their prowess in the markets by actively trading in the short term. However, instead of focusing on the long-term impact on their clients, they may be creating gaps or blind spots. Often, they are not servicing your account and allow positions to become dangerously overweight by chasing what's running, thereby eroding the quality of your diversification strategy.

Rather than trading short-term investments often, we take a different approach. Instead, we look at holding securities long enough to get preferential tax rates while staying diversified in our investments.

Advisor Tip: Work with Someone Focused on a Comprehensive, Long-Term Approach

There are several reasons we prefer this approach. For one, we believe in a long-term strategy focused on time in the market rather than timing the market. A good advisor doesn't just look at performance as an increase or decrease in a portfolio's value. Instead, when markets run, a good advisor turns to research-backed strategies such as target band rebalancing and tax-loss harvesting to capitalize on opportunities for their clients. Additionally, a good advisor should be able to explain both the asset allocation and asset location strategies they recommend and why it's best for your situation. For example, is the right mix of stock and bond exposure to help you sleep more easily at night? Is there newly available research from the firm's leaders on investments and the markets? What are the current prevailing market conditions? If the investment recommendations you receive don't incorporate these considerations, it would be wise to seek a second opinion.

Red Flag #8: No Designations

Meteoric growth in the financial services industry has predicated advisors' desires to possess a competitive "edge" that helps them stand out amongst the competition. As a result, there are a host of designations that advisors can have, but they are not all created equal. The most prestigious and valuable designations are CFA®, CFP®, CIMA®, CPA, J.D., and MBA/Ph.D. in Finance.

Meteoric growth in the financial services industry has predicated advisors' desires to possess a competitive "edge" that helps them stand out amongst the competition. As a result, there are a host of designations that advisors can have, but they are not all created equal. The most prestigious and valuable designations are CFA®, CFP®, CIMA®, CPA, J.D., and MBA/Ph.D. in Finance.

A lack of designations often reflects an advisor's desire to prioritize their time making sales instead of expanding their knowledge of financial planning techniques and investment management strategies- a fact that should rightfully give you pause.

Red Flag #9: Tarnished BrokerCheck Record

Of any warning signs on this list, having a tarnished BrokerCheck record is the most concerning. BrokerCheck is a free online tool hosted by FINRA that allows you to look up the record of any financial professional with a securities license. If an advisor has a blemish or disclosure on their record, it may be a sign that they have operated unethically or illegally in the past. Often, these disclosures indicate that a professional was disciplined previously for violating either their firm's, the SEC, or both parties' guidelines. When considering the professional you want to work with, we strongly encourage staying away from advisors with misconduct on their BrokerCheck record.

How to Find a Fiduciary Financial Advisor to Work With

Knowledge is power, so understanding the topics mentioned above is crucial when evaluating an advisor.

At WJA, our team of disclosure-free advisors looks at the full picture when making financial recommendations for our clients. We look at investments and insurance as important pieces of the plan much like employee benefits and taxes. Additionally, we don’t sell products or make commissions, so we’re on the same side of the table as our clients when we give guidance.

While some of these red flags seem minimal, others are more concerning. For example, a blemished Brokercheck record is more a cause for concern than if your advisor-sold mutual funds to you. However, if your current or prospective advisor tries to push you only towards high-fee or commissioned products, you may benefit from seeking another opinion from a fee-only RIA, or a fiduciary advisor.

When it comes to our firm, our mission is to give great advice in your best interest, 100% of the time.