And just like that, it's tax time again! Every spring, our in-house tax team gears up with excitement. However, most high-income professionals approach tax season with dread, exhaustion, and confusion. Typically, many individuals fall into two brackets:

- those who want to get taxes done as quickly as possible, and

- those who procrastinate because they don't want to deal with it at all.

Whichever bracket you fall into, many of us can agree that we hate filing our taxes and just want it to be over and done with. Whether you're a procrastinator or an early bird, each approach can cause stress between you and your tax preparer as they work on your tax return. Those who want their tax return done as quickly as possible often tend to impose unrealistic expectations on the CPA, and those who procrastinate and provide last-minute information to the preparer – expecting it to be done by the April deadline – are creating an almost impossible situation. Neither scenario ends with a good relationship between you and your CPA.

However, there's an important option to remember as we near the April deadline that can help alleviate this stress – while tax payments are still due each April, you can elect to extend your return until the October deadline by filing an extension. We don't often hear about tax extensions or their benefits, so let's dive into why this option can be a great and underrated choice for many high-income professionals.

Why Should I File a Tax Extension?

When discussing tax extensions with our clients, we're often met with initial hesitation or concerns.

"Will I get flagged for an audit?"

"Will the IRS charge me more if I turn it in at a later date?"

"Can't we just rush the return to get it over and done with by April?"

We'll discuss many of these concerns throughout this article, but the simple answer to these questions is that it's simply in a client's best interest to extend their returns to give the necessary due diligence and review it deserves.

In the last several years, we've seen an annual decrease in young professionals pursuing tax accounting as more seasoned professionals begin to retire. Historically, tax accounting has been a grueling profession—hours upon hours of miserable overtime, demanding clients, and no work-life balance. Who can blame young CPAs for wanting to count inventory rather than prepare tax returns? While the state of the profession is an alarming trend, what it means for high-income professionals is that there are fewer experienced CPAs to handle the demand for increasingly complicated tax returns and tax planning needs. Moreso, it means that the few CPAs entrusted with these returns are stretched thin from January to April.

Avoid Late Penalties and Reduce Error

One benefit of tax extensions is simple—no one wants errors on their tax return, and tax returns take time to prepare accurately. Even if you think it's an easy return, you want your CPA to take time with your return to provide a thorough review of your materials and diligently prepare it. Your CPA has specific processes to decrease the risk of error in your return and usually has hundreds of tax returns to complete. These processes all take the scarcest resource available to all of us: time.

These processes include but are not limited to the following -

- They are accessing client documents and collating them into standard work paper format. A fundamental principle is that accountants standardize everything for better documentation. This takes time, even if this process is implemented by automation software.

- Preparation of the return. The client information is input into the tax software.

- Review of the return. The tax profession's due diligence standard requires an inspection to ensure the tax return has been prepared correctly and that no information has been excluded. Your CPA also wants to ensure that any positions taken on your return will have a level of success if questioned by the IRS.

Rushing these processes increases the chance of errors. Choosing an extension is an excellent way to ensure that your return is correct because your CPA will have more time to spend on your return.

During my years in this profession, I've had a few clients tell me that they know how quick it is to prepare a tax return since they prepared it themselves. I always respond by pointing to our due diligence standard – for every return we work on, straightforward or complex. We have a requirement to exercise a review of the information and positions on the return.

Interest & Tax Penalties in a High-Interest Rate Environment

One conversation we’ve had with many clients surrounds tax penalties and interest. Remember, tax returns can be extended to the October deadline, but payments MUST be made by the April tax deadline each year. There are a few types of penalties you could see if your tax payments are late, but what’s more important is to realize that the interest you pay on any unpaid tax is the federal short-term rate plus three percent and is determined by the IRS quarterly.

For tax underpayments or overpayments in the second quarter of 2024, interest will be 7% per year, compounded daily.

Many people don’t realize that the higher-for-longer interest rate environment we’re seeing has widespread implications, including tax payment interest. While most understand the impact high rates have on mortgage rates or some fixed income investments, the interest charged on tax underpayments catches many off guard when the letter from the IRS arrives in the mailbox.

Another surprise? The IRS will use any payment you make to cover the tax itself first, then any penalties, and finally the interest. So, interest can continue compounding at these high rates if you make partial or delayed payments. To avoid the compounding effects, our tax team works closely with our advisors to assess client’s cash flow for tax payments, projected rates, interest and penalties, and how to navigate making their tax payments in the most effective way possible.

Filing an Extension Creates Extra Time to Navigate Changing Tax Laws

Many changes have happened in the tax profession over the last 25 years. Most years, there are midnight December 31st laws passed that often introduce increasingly complex tax laws (even if disguised under the term "simplification") for the upcoming tax season. We've even seen tax laws change in the middle of tax season!

Unfortunately for CPAs everywhere, we can assume that this pattern will continue. Being prepared with a tax extension can give you and your CPA time to implement these laws and get the most out of your tax return. Listed below are three end-of-year changes that impact you and your tax return.

- A law change always impacts a tax form.

- The IRS has to update the tax form.

- The software programmers have to program the form changes into the software.

If there has been a tax law change, this will trickle down to a change in a tax form. As these laws inevitably change, a tax extension allows sufficient time to learn the new rules and make these changes.

Advisor Insights: While these behind-the-scenes changes are happening, CPAs and advisors work diligently to understand how the changes impact existing laws, contribution limits, and financial strategies to find the best path forward for clients.

In addition to these law changes, someone at the IRS has to re-design the tax form to account for the recent law change. This takes time, especially considering the IRS is understaffed. Once the IRS finalizes the form, the tax preparation software programmers burn the midnight oil on the back-end software system to ensure the form changes are implemented, tested, and calculated correctly. This process can be time-consuming and frustrating for everyone involved – CPAs, people trying to finalize their return, and everyone putting the change in place. However, rather than getting caught up in the mess of change, having an extension to fall back on can create some ease of mind.

Let's take a look at an example to explain the potential timeline.

On March 11, 2021, Congress enacted a law that exempted the first $10,200 of unemployment benefits from taxation and made it retroactive to 2020 tax returns. Unfortunately, by mid-March, many individuals had already filed their 2020 tax returns. To take advantage of this tax break, they needed to file amended returns, which can be lengthy and cumbersome.

For those who had not yet filed, they had to wait for the following to be completed and tested before submitting their return by April 15th:

- guidance from the IRS on how this change was to be presented on the 2020 tax return,

- software programmers to put the IRS guidance into code, and

- final testing to ensure the software was accurately computing the law change.

Only then could the tax preparer finish the returns of those impacted. Additionally, if you fell into this group of people looking to take advantage of the tax break, there was nothing your CPA could do to produce your return any quicker. The CPA couldn't call the IRS or software programmers to speed up the process. No amount of daily phone calls asking when your return will be finished or round-the-clock emails wondering if your CPA has forgotten you could get your return stamped and sent. This was simply beyond your CPA's control.

Long story short, the earlier you file your tax return, the greater the risk of tax software incorrectly computing your tax return, especially as laws evolve. Here at WJA, we receive weekly (and sometimes daily) updates to our software clear into April. So, extending the time to file is an excellent solution to the flood of early-year software updates.

Additional Review for Tax-Minimization Opportunities & Financial Planning

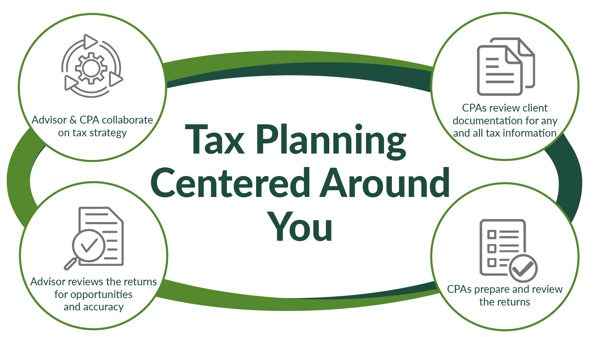

At Willis Johnson & Associates, our team of in-house CPAs works year-round with our financial advisors to provide ongoing tax planning knowledge and stay apprised of the financial strategies leveraged in each client's unique financial plan. This collaborative approach has many benefits, however, in our due diligence and collaboration, it's seen most plainly.

For each tax return handled by our tax team, our advisors do an in-depth review to assess opportunities for additional tax minimization or future financial planning. This collaboration enables a 360-view of a client's tax situation and gives perspective from throughout the year to incorporate into the returns: did the clients buy a house, do a Backdoor Roth conversion, or buy a rental property? What are their goals for next year? Did they see significant gains or losses this year that we can use to offset future ones?

Our advisors are also cross-trained in the common tax mistakes we often see Shell, Chevron, and BP employees making, so they can identify potential issues for the tax team to watch out for before W-2s and other documents roll out. This added review increases the turnaround time for your tax return but is essential to ensure all pieces of your financial puzzle are working together.

Additionally, by getting the full picture of an individual's situation rather than just what's on the documents provided, our team is equipped to ask the right questions to get the most accurate information for each return.

A Tax Extension Results in More Information Available to You

By delaying the filing of your tax return, you will have more information for tax planning. This enables better tax planning for your unique circumstances. Extending the time to file is an excellent solution for achieving short-term and long-term tax planning.

Let's illustrate this with an example.

Say that your return for 2024 has been preliminarily prepared and reflects an overpayment of tax. You can refund this or apply it to 2025 estimated tax payments. In the first quarter of 2025, you aren't anticipating any significant tax events. If you file your return before April 15, you will select a refund because you and your spouse want to take a cruise with the refund.

However, your CPA requests that you obtain an extension instead. In late July of 2025, the market takes a nose dive, and your financial advisor decides that this is the perfect time to perform a Roth conversion of a portion of your traditional IRA. Doing so will create tremendous growth in the Roth over time, leading to a much larger tax-efficient nest egg at retirement. But, this conversion will generate additional tax due for 2025.

Because you filed an extension, you now have the opportunity on your return to apply the overpayment of 2024 taxes to the 2025 estimated tax generated by the Roth conversion.

Had you filed before April 15, opted for the refund, and taken the cruise, you would have to find extra cash to make an estimated tax payment for the Roth conversion. And, if there wasn't a readily available stash of cash to do so, you may have to forego the Roth conversion, which would be a less-than-ideal long-term financial decision.

There are other ancillary reasons to postpone filing. For example, banks, lenders, and brokerages are issuing more and more corrected tax documents well into March and April. If you file your return before receiving a corrected tax document, you will have to pay your tax preparer twice:

- The first time — To prepare for your return the first time, and

- The second time — To prepare an amended return.

That's double the tax prep fees. Who wants that?

And if you've heard that filing an extension increases your risks of an IRS audit, I want to put your mind at ease. There are no statistics to support that rumor. Suppose your return is prepared correctly by your CPA, who has taken the time for due diligence and reported all the corrected documents with fully updated software. In that case, you have no fear even if your return is selected for audit. All the more reason to say "yes" to your tax professional when they suggest filing an extension.

How to File a Tax Extension

If, after reading the benefits above, you've decided to file an extension for your taxes, there are a number of ways to get started. On the IRS website, you can find several resources, deadlines, and detailed information on how to file an extension based on your filing status.

A key caveat to keep in mind is that while you may file an extension for your return (typically to a date in October), the payment is still due by the April tax deadline. If you have any questions, your tax preparer should be well-versed in this process and be able to answer them.

Tax Planning & Preparation Alongside Your Financial Plan

At Willis Johnson & Associates, we're firm believers that tax planning is an essential component of any financial plan. Each tax season, our team of in-house CPAs and experienced contract accountants work around the clock to ensure that our clients receive the utmost level of attention and care given to our client's returns. However, extensions are a crucial part of our process to leverage tax planning and mitigation strategies over time and to ensure accuracy for each return. More than that, for some clients, we also believe it's in their best interest to extend returns so we can get additional information on their tax picture as detailed documentation rolls out in later spring months.

If you're interested in learning more about our incorporation of tax planning into the financial plans we create for our clients, you can learn more about our process here or schedule a complimentary meeting with a member of our team.