Featured Post:

How Waiting 15 Days to Retire May Save You Thousands in Taxes on Your BRP Payouts

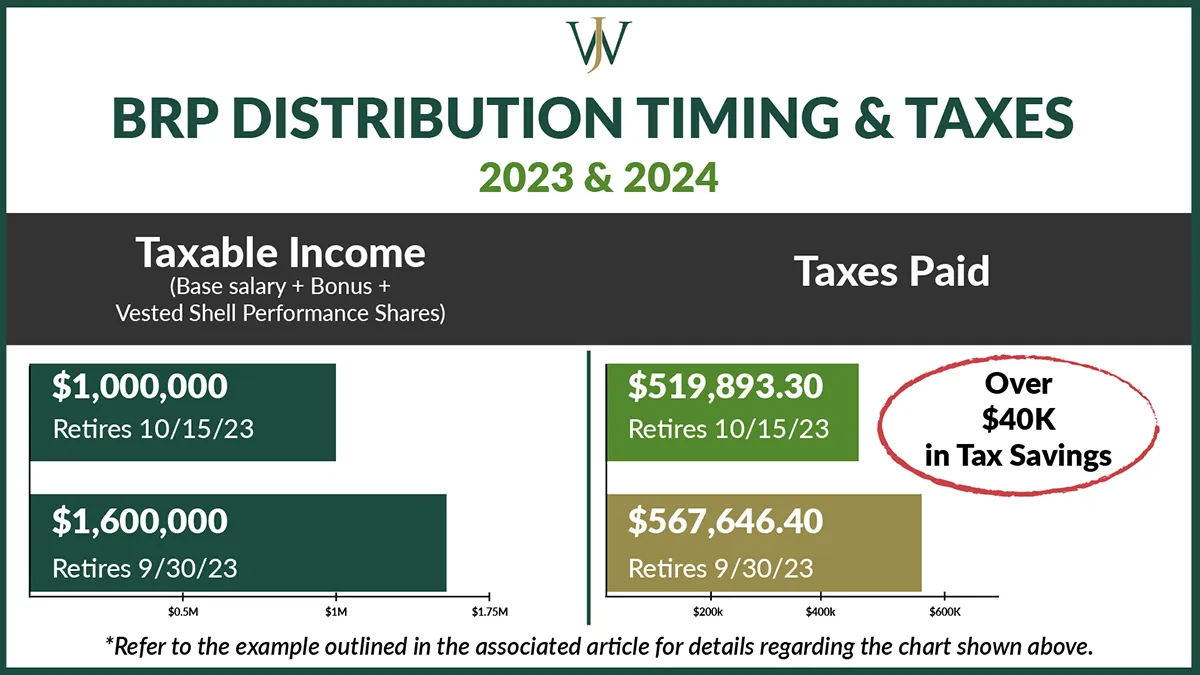

I was recently working with a Shell executive client, let’s call her Lynn, who had been putting in long hours on a challenging assignment and was ready to retire by September 30, 2025. I worked with...