Featured Post:

Improve Your Investment Strategy With Target Band Rebalancing

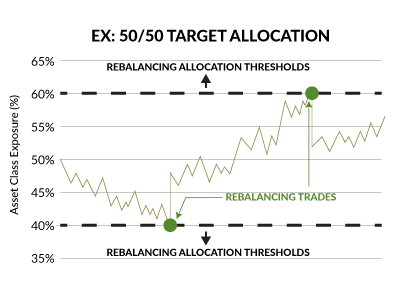

When asked about the best ways to invest, people offer a variety of responses. Inevitably, many of these responses boil down to "buy low, sell high." Charmed by its deceptive simplicity, investors...