A Quick Guide to Shell Retirement Benefits for Hire Dates Between 2006 and 2017

During the working years of life, healthcare premiums are a familiar part of the regular routine. Monthly costs are automatically deducted, and Open Enrollment periods allow workers to review and make necessary adjustments each year. Understanding retirement healthcare benefits become a little more convoluted.

When it comes to understanding Shell retiree health insurance, rumors, and water cooler talk won’t cut it. Employees need a clearer understanding so they can plan accordingly and maximize their benefits. You need to plan for many things around the transition to retirement, and healthcare is just one of them.

This article is intended to clear up confusion for Shell employees or retirees who were hired or rehired between January 1, 2006, and January 1, 2017. For those that were hired or rehired prior to January 1, 2006, please see this article.

When Does Shell Retiree Health Insurance Start?

Shell offers medical, dental, and vision benefits to retirees that meet one of the following criteria at termination:

- Be at least 50 years old and have 80 points (years of eligible service + your age) or

- Age 65 or older and eligible for a Regular Pension or

- Eligible for disability pension (any age) or

- Satisfy 70-point Eligibility rules

To uphold the 70-point rules, you need to be at least 50 years old, possess 20 or more years of eligibility service, and have your termination attributed to specific circumstances such as severe illness, the sale or closure of a facility/ office/plant, the sale or dissolution of a participating company, or the restructuring of the workforce of a participating company. See Summary Plan Description, pages M-10, for details

Health Insurance Options Beyond Shell Retirement Benefits

What happens if your employment is terminated and you do not meet one or more of the eligibility requirements? If you don’t meet the plan requirements, you have alternative options for healthcare coverage in retirement.

Using COBRA for Insurance Coverage

The Consolidated Omnibus Budget Reconciliation Act of 1985 (COBRA) allows you and your dependents to continue medical, vision, and dental coverage for a limited time if you experience a qualifying event that causes the loss of company health insurance. Retirement and termination (except in cases of gross misconduct) may qualify as events.

To take advantage of COBRA, you must choose it within 60 days of receiving notice. The maximum coverage period is typically 18 months, but certain circumstances, such as disability, can extend the timeframe. Under COBRA, you are responsible for the entire cost of coverage (Shell does not provide a subsidy), and there’s an additional 2% administration fee.

Here is what you need to know about COBRA coverage:

- Can continue medical, vision, and dental coverage.

- Must elect COBRA within 60 days of notice.

- Time-limited coverage of 18 months, except in certain circumstances.

- The cost of coverage is your full responsibility, plus 2% fee.

Purchasing Insurance Through the Healthcare Marketplace

Another option available is purchasing coverage for yourself and your dependents through Healthcare.gov, the US Government Healthcare Marketplace established by the Affordable Care Act. It provides private health care coverage.

When you choose this option, you will be responsible for the entire cost of coverage. However, depending on income level, you may qualify for “premium tax credits” the federal government offers. These tax credits can help reduce the cost of coverage.

Here is what you need to know about marketplace insurance:

- Multiple options are available through the Healthcare Marketplace.

- Offers private healthcare coverage.

- You pay the premium.

- Premium tax credits may reduce costs.

When comparing the options, it’s important to note that COBRA coverage may come with higher costs compared to purchasing coverage on the Marketplace. However, it can still be a viable choice if you’ve already met your deductible on Shell’s plan.

It’s also worth mentioning that the Marketplace offers potential benefits, especially for individuals with lower incomes who may qualify for federal subsidies. These subsidies can help alleviate the financial burden of healthcare coverage.

What Does Shell Retiree Health Insurance Look Like Before Age 65?

Assuming you meet the retiree company health insurance criteria, it’s important to understand what the coverage entails. In many ways, it resembles the medical coverage you had while working.

Until you’re eligible for Medicare, typically at age 65 (but may vary depending on certain medical situations), you and your dependents remain eligible for the same medical coverage as active employees. This includes the option to make changes during open enrollment periods.

During pre-Medicare coverage, your insurance benefits look the same as when you were employed. The continuity of coverage helps provide a smooth transition into retirement, ensuring that your healthcare needs are met. Options include:

Medical Plan Options (before Medicare)

- PPO – United Healthcare

- High Deductible Healthcare Plan (HDHP) - United Healthcare

- Kelsey-Sebold Greater Houston Plan

- Regional Health Maintenance Organization (HMO) and PPO options are available in some areas

Paying Your Premiums

Similar to when you were working, your premiums can be deducted from your pension payment or, in certain cases, paid by invoice or an automatic bank withdrawal.

Healthcare Savings Accounts (HSA)

Like when you were employed, upon retirement, you can still pair the High Deductible Health Plan (HDHP) with an HSA. If you are covered by an HDHP until the age of 65, you have the opportunity to make tax-deductible contributions to an HSA (up to $7,350 family contribution annually).

Unlike a Flexible Spending Account (FSA), the HSA does not have a use-it-or-lose-it policy. Contributed funds can be withdrawn and used for qualified medical expenses without incurring tax.

Investing HSA Funds: Alternatively, you can choose to invest the funds for potential tax-free growth as long as the withdrawals are used for qualified medical expenses. This presents an advantage for those who find high-deductible plans suitable.

Withdrawal Penalties: Withdrawing HSA funds for non-medical expenses will likely result in taxes on the distribution, along with a 20% penalty for those under age 65. However, at age 65, the HSA functions similarly to an Individual Retirement Account (IRA) without an early withdrawal penalty.

Despite being relatively lesser-known and underutilized, the HSA can serve as a valuable financial tool. For more information on whether the HDHP and/or HSA align with your specific circumstances, click here.

Company Health Insurance and Medicare After 65

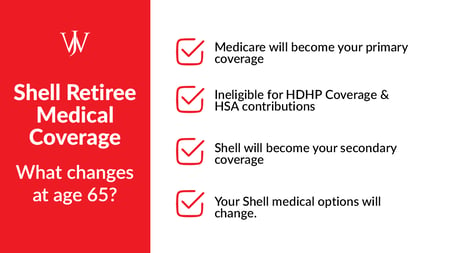

Once you are eligible for Medicare (which is typically at age 65, but could be earlier under certain circumstances), your coverage will change in several important ways.

Medicare Becomes Your Primary Coverage

Visit SSA.gov/Medicare to apply for benefits starting 3 months prior to your 65th birthday. You have a 7-month enrollment window. If you fail to sign up during this period, you risk permanently increased premiums that may continue to go up if you wait to enroll.

Advisor Note: You will need to be enrolled in Medicare Part A and Part B BEFORE enrolling in one of the Shell plan options as your Shell coverage will be secondary to Medicare.

Change in Shell Medical Options

The following plans are available to Medicare-eligible retirees:

- Shell Medicare Advantage PPO

- KelseyCare Advantage PPO

- Other Regional Medicare Advantage and Supplement options may be available in some areas.

- Please note the Shell Medicare Complementary plan is no longer available to new enrollees

No Longer HSA-Eligible

Once you become Medicare eligible, you lose eligibility for coverage under a high-deductible health plan. As such, you can no longer contribute to an HSA account.

Who's Financially Responsible for Insurance Premiums After Your Shell Retirement?

As a Shell employee, the payroll department probably took care of your premiums. Now that you’re not on a payroll, figuring out who pays for what can be confusing. Here’s a basic rundown of financial responsibility.

Vision & Dental Coverage Contributions

When it comes to vision and dental, you will be responsible for covering the full cost of these services. This means that the premiums for vision and dental plans remain your sole financial obligation.

Medical Coverage Contributions

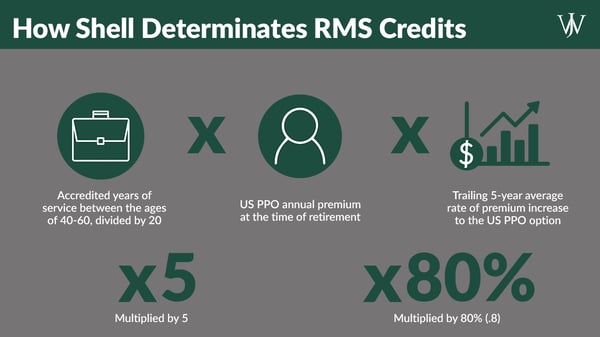

For Shell employees hired or re-hired after January 1, 2006, Shell will establish a Retiree Medical Supplement Account (RMSA) at the time of your retirement to help defray the cost of medical coverage premiums.

Determining Shell’s Contributions - The contribution, often referred to as ‘credits,’ from Shell’s end will be determined at the time of retirement. Several factors influence this calculation, including the current cost of the US PPO plan, recent premium rate increases, and years of service.

Exceptions for Disability Pension: If you retire on a qualified disability pension, Shell extends additional support. You will receive the maximum company subsidy for retiree medical premiums until age 60. At this point, your Retiree Medical Supplement Account will be established, and credits will be determined as if you worked until age 60.

Making the Most of Your Shell Retiree Medical Supplement Account (RMSA)

The credits in your RMSA are only available to subsidize the cost of retiree Shell Medical coverage for you or your dependents and cannot be passed to an estate or beneficiary. The credits will not increase in value over time (non-interest bearing), so use them!

Each year, during Open Enrollment, you will select how many credits you would like to use in 10% increments (from 0% to 80%) toward your retiree medical premiums. The percentage is in relation to the total premium cost.

For example, let's assume coverage costs $600 per month, and during Open Enrollment, you elected to use your RMSA credits to pay for 80%. Each month, $480 worth of credits would be withdrawn from your RMSA, and you would be responsible for the remaining $120, or 20%.

Once your RMSA credits are exhausted, you will be responsible for 100% of the retiree medical premiums thereafter. The length of time your credits last will be dependent on which coverage plan you select (for example, the HDHP has a lower premium cost than the PPO option) and what percentage you elect to use each year (the higher the percentage, the fewer years your credits will last).

How Immediate Eligibility Impacts Medical Coverage at Retirement

Retirement planning from Shell involves many factors beyond your control, such as healthcare costs and the rate of premium increases. However, what you can (typically) control is your years of service at Shell.

Let’s consider Roger, who is 60 years old and started with Shell later in his career at age 43 in 2007. He will have completed 17 full years of service at the end of 2023. If he leaves Shell this year, is he able to enroll in medical coverage under the Shell plan?

Maybe – the answer isn’t straightforward. Unless Roger qualified for a disability pension, he may not meet the age requirement for other eligibility criteria. However, in the event that he does qualify for a disability pension, Shell would take into account his entire 17 years of service when calculating his RMSA credits.

Without the disability pension, the earliest age at which Roger could retire with eligibility for Shell retirement benefits is 62. This is the point at which Roger has accumulated a total of 80 points, combining his age and now 19 years of service. It’s worth noting that beyond age 62, Shell’s contribution to Roger’s retiree medical coverage would not increase.

How a Fiduciary Financial Advisor Can Help Optimize Your Retirement Timing from Shell

The retiree medical benefit plan is just one of many factors that play into your retirement planning strategy after Shell. Balancing health insurance premiums and coverage needs against your other savings and goals for retirement in a tax-efficient manner can play a huge role in your satisfaction during your golden years.

Willis Johnson & Associates has extensive experience collaborating with Shell professionals and executives to provide expert guidance in aligning all factors associated with retirement. Learn more about the ways we support Shell employees through the retirement journey, or contact us to see how we can help you get started.