Healthcare is one of the most common benefits for working employees. And for Shell retirees with a hire date prior to 2006, these benefits can continue well into your golden years. However, healthcare benefits change slightly when you leave the workforce.

This article covers everything that you need to know about healthcare options for Shell retirees. Specifically, we’ll discuss benefit options for retirees with a hire date before January 1, 2006. For those hired after this date, please see this article.

Who Is Eligible for Shell Retiree Coverage?

Shell offers medical, dental, and vision benefits to retirees that meet one of the following criteria at termination:

- Be at least 50 years old and have 80 points (years of eligible service + age)

- Age 65 or older and eligible for a regular pension

- Eligible for disability pension (any age)

- Satisfy 70-point eligibility rules

For example, if an employee is at least 50 years old and they have 20+ years of eligible service, they may receive retiree benefits coverage when termination is due to factors like poor health, the closing of a facility, or the participation in a workforce reduction layoff.

Please note: Shell retiree coverage is not available for those hired or re-hired after January 1, 2017.

What Are Your Options if You Don’t Qualify for Shell Retiree Healthcare Coverage?

If you do not meet one of the criteria at termination, you may still receive healthcare coverage through COBRA temporary coverage or by purchasing a plan on the Healthcare Marketplace.

COBRA Temporary Coverage

The Consolidated Omnibus Budget Reconciliation Act of 1985 (COBRA) allows terminated employees to continue employer-sponsored healthcare coverage for a limited amount of time following a qualifying event.

Retirees must make a COBRA election within 60 days of termination. In most cases, the maximum coverage period extends up to 18 months. This may be extended during periods of special circumstances or as the result of a disability determination.

Individuals are responsible for the entire cost of coverage, including a 2% COBRA administration fee. Shell does not subsidize COBRA premiums.

Healthcare Marketplace Coverage Through the Affordable Care Act

A variety of individual and family plans are available through the Healthcare Marketplace. This US government-subsidized coverage is provided through the Affordable Care Act (ACA), which aims to make healthcare coverage more accessible and affordable to all.

Marketplace plans are private insurance plans. Individuals are responsible for all costs, including premiums and administrative fees. Shell does not subsidize marketplace plans. However, some individuals may be eligible for an income-based subsidy or tax credit from the US government.

What Does the Shell Retiree Healthcare Plan Cover?

The Shell Retriee Healthcare plan is designed to bridge the gap between your termination date and the date when you become eligible for Medicare. In most cases, this is your 65th birthday but may vary based on individual circumstances.

The Shell Retiree Healthcare Plan works like the employee plan you are most familiar with. There is an Open Enrollment period where you can make changes to your coverage, plan options to meet specific needs, and a healthcare savings account to help you cover the cost of care.

Medical Plan Options (before Medicare)

- PPO - United Healthcare

- High Deductible Healthcare Plan (HDHP) - United Healthcare

- Kelsey-Sebold Greater Houston Plan

- Regional Health Maintenance Organization (HMO) and PPO Options

Premiums for elected coverage can be deducted from pension payments or paid by invoice or automatic bank withdrawal.

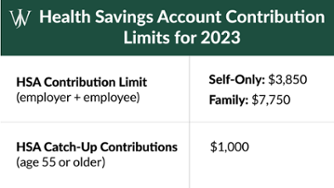

Health Savings Accounts

Another similarity is the option to participate in a health savings account, often paired with the High Deductible Health Plan (HDHP). Any year(s) you are covered by an HDHP before age 65, you may make annual tax-deductible contributions to your health savings account, or HSA.

HSA funds can be withdrawn and used for qualified medical expenses, making them completely tax-free. Or, these funds can be invested for tax-free growth. You will pay taxes on the distribution and up to a 20% penalty if making withdrawals before age 65, effectively making the HSA operate like an IRA.

Please Note: There is an annual maximum for individual and family contributions. Please check the maximums for the current tax year.

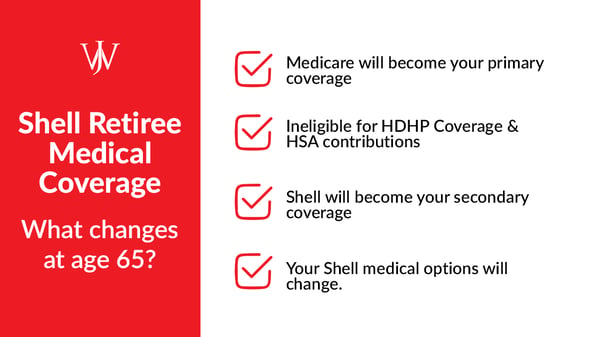

How Shell Retiree Healthcare Coverage Changes at Age 65

Once you are eligible for Medicare (which is typically at age 65, but could be earlier under certain circumstances), your coverage will change in several important ways.

Medicare Becomes Your Primary Coverage at Age 65

When you turn 65, Medicare becomes your primary coverage, and the Shell Retirees plan becomes secondary coverage.

You will have a 7-month enrollment window around your 65th birthday (3 months prior, your birthday month, and 3 months following) to apply for Medicare. Visit SSA.gov/Medicare to enroll online.

Advisor Tip: Be sure to apply within the three months prior to your birthday month in order to avoid any lapse in coverage.

If you fail to sign up after your initial 7-month enrollment window (and do not have other primary coverage), a penalty applies, which will permanently increase your Medicare premiums.

You will need to be enrolled in Medicare Part A and Part B before enrolling in one of the Shell plan options.

You Will Select a New Shell Retiree Medical Plan

Your coverage options change when the Shell Retiree coverage becomes your secondary plan. Here are the plan options available to Medicare-eligible retirees:

- Shell Medicare Advantage PPO

- KelseyCare Advantage PPO

- Other Regional Medicare Advantage & Supplemental Options (Regional Availability)

Please Note: Shell Medicare Complementary Plan is no longer available to new enrollees.

You are No Longer Eligible to Participate in an HDHP (or HSA)

Once Medicare becomes your primary coverage, you are no longer eligible to participate in a high deductible health plan (HDHP) and will also no longer be able to contribute to a health savings account.

Who Pays for Shell Retiree Health Coverage?

Now that you know how to qualify and what coverage is included, comes the big question – who pays the premiums?

Vision and Dental Coverage

The individual pays for the full cost of vision and dental coverage premiums. Shell does not subsidize these plans.

Medical

Shell will share in the cost of the premiums for medical coverage for retirees hired or re-hired prior to January 1, 2006. Shell’s contribution depends on the maximum value of company subsidy and your years of service.

- For non-Medicare-eligible retirees, the maximum value of company subsidy is calculated based on 80% of the US PPO plan cost

- For those eligible for Medicare, the maximum value of the company subsidy is calculated based on 80% of the Medicare Complementary option.

Your full years of accredited service determine how much of this maximum company subsidy you receive.

|

Full Years of Accredited Service

|

Shell premium Contribution

|

Participant’s Portion* (of US PPO premiums)

|

Shell’s Portion* (of US PPO premiums)

|

|

30+

|

100% of maximum subsidy

|

20% of premiums

|

80% of premiums

|

|

29

|

95% of maximum subsidy

|

24% of premiums

|

76% of premiums

|

|

28

|

90% of maximum subsidy

|

28% of premiums

|

72% of premiums

|

|

27

|

85% of maximum subsidy

|

32% of premiums

|

68% of premiums

|

|

26

|

80% of maximum subsidy

|

36% of premiums

|

64% of premiums

|

|

25

|

75% of maximum subsidy

|

40% of premiums

|

60% of premiums

|

|

Over 10, but less than 25

|

70% of maximum subsidy

|

44% of premiums

|

56% of premiums

|

|

Less than 10

|

None

|

100% of premiums

|

None

|

|

*Participant’s portion could be a smaller percentage, and Shell’s portion could be a larger percentage if using the HDHP plan, as the premiums are less compared to the PPO plan.

|

|||

Retirement Planning & How to Time Retirement to Maximize Benefits

There are many factors that are out of your control. The cost of healthcare, premium increases, and coverage all factor into the value of Shell Retiree Health Plan coverage. One factor that employees can often control is their length of service and when they retire, which directly impacts plan coverage and cost.

For example, a 49-year-old employee leaving the company after 27 years of service may not be eligible for a retiree plan. But if that same employee waits two more years to leave at age 51, he or she will likely meet the eligibility criteria of being at least 50 years old and 80 points for years of service.

Working with a Fiduciary Financial Advisor When Starting Your Shell Retiree Health Plan

The decision on when to retire is complex. There are many factors to consider, including how long you have been employed and whether or not an additional year or two will make a difference in your eligibility. If you need help balancing your insurance, pension, and other benefits, we can help you evaluate your options to make sure you are not leaving anything on the table. The advisors at Willis Johnson & Associates have worked with hundreds of Shell professionals and are experts at helping align the competing factors that come along with retirement.