You’ve worked hard for your retirement. After a long career at Chevron, you deserve to enjoy your retirement to the fullest. A big part of maximizing your retirement enjoyment depends on skillfully planning the disbursement of your benefits.

To maximize your Chevron retirement benefits and efficiently minimize your overall tax burden, it’s important to strategically choose your retirement date. While no one specific date works for everyone, we’ve outlined a number of factors that could potentially affect your retirement, so you can determine the best date for you to retire from Chevron.

What Factors Should I Consider When Selecting My Chevron Retirement Date?

The calculations for several of your Chevron employee benefits may vary depending on the year or the time of year when you begin receiving them. Some examples of benefits to take into consideration include:

- Your 401(k), the Chevron Employee Savings Investment Plan (ESIP)

- Your bonus, the Chevron Incentive Plan (CIP)

- Your Qualified Pension, the Chevron Retirement Plan (CRP)

- Your Non-Qualified Pension, the Chevron Retirement Restoration Plan (RRP)

![]()

Chevron Employee Savings Investment Plan (ESIP)

No matter when you plan to retire, focus on maximizing your 401(k) contributions during your final years of work. How much you can contribute to your ESIP depends on your age. For 2026, the breakdown is as follows:

- If you're under age 50, the maximum amount you can save in your 401(k) is $72,000. This includes contributions you make to pre-tax, Roth, or after-tax sources as well as what Chevron contributes on your behalf.

- As an employee over 50, you can put $32,500 pre-tax or roth into your 401(k) in 2026 and can also make after-tax contributions. When employer contributions are included, the threshold increases to $80,000 for 2026 if you're 50 or over.

- Employees aged 60 to 63 after January 1, 2026, can contribute even more to workplace retirement plans thanks to legislation under Secure Act 2.0. Instead of the standard catch-up amount of $8,000 for individuals over age 50, savers aged 60-63 can leverage a catch-up amount of $11,250 in 2026 to boost their retirement savings.

If you’re expecting to retire at the beginning or middle of the year, you’ll want to boost your contribution percentages early that year. Strategically contribute higher percentages of your salary and bonuses in the first quarter to maximize your contributions and Chevron’s employer contributions.

Learn how to max out your Chevron 401(k) here >>

Chevron Incentive Plan (CIP)

Many people consider their bonus a key factor in when to retire; it’s common to see employees decide to work through the end of the year to receive their full performance bonus.

However, several different factors may influence whether it’s worth it to schedule your retirement date around your bonus.

- Bonuses are paid out in March for work done in the prior year. You may retire before March and still receive your full performance bonus for the previous year.

- If you only worked a portion of the year, your bonus amount is at Chevron’s discretion. Typically, employees receive a prorated bonus based on quarters of employment. You must have worked at least one day in the following quarter to be eligible for a prorated quarter of bonus benefits. For example, the first quarter ends on March 31; you must still be employed on April 1 to receive a 25 percent prorated bonus.

- Your bonus will be taken into consideration when calculating your pension, so the date you choose can have an impact on your total pension benefit.

![]()

The potential impact on your pension’s value can be the biggest determining factor when deciding whether to plan your retirement date around your bonus.

Chevron Retirement Plan (CRP)

Your Chevron Retirement Plan pension can be paid to you as either a lump sum rollover to an IRA or a monthly annuity. Your retirement date plays a significant factor in determining the total value of your CRP.

If you choose the lump sum option:

Many Chevron retirees choose the CRP lump sum option so they have the power to invest their pension funds at their own discretion.

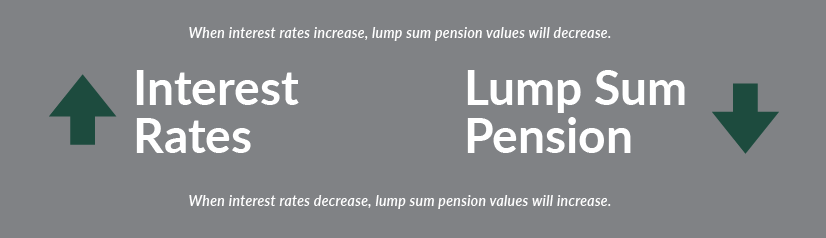

The interest segment rates Chevron uses to calculate the lump sum change every month. If interest rates go down, the lump sum value goes up and vice versa.

When you retire and decide to start your pension benefit determines which set of interest rates are used for the calculations, so keeping an eye on rates and factoring them into your retirement date planning can be wise.

Reflecting back on the bonus discussion, delaying your retirement to boost your bonus can affect the pension calculation rates and your total pension amount; compare the two to make sure you’re choosing the wisest option.

Get An Idea of Your Chevron Lump Sum Pension Calculation Using Recent Segment Rates Here >>

If you choose the annuity option:

The annuity pension provides ongoing income. It can be started immediately or deferred until a later date. Choosing to defer this income can often make sense, depending on the other multiple income streams you’ll receive around retirement.

Depending on the time of year you retire and the date you choose to receive different funds (severance, unpaid benefits, 401(k) and IRA disbursements, etc.), delaying your annuity payments to a different calendar year may have a positive impact on your tax planning.

Chevron Retirement Restoration Plan (RRP)

Some Chevron employees may also participate in a non-qualified pension plan called the Chevron Retirement Restoration Plan (RRP).

The default payment method is a lump sum paid during the first quarter that’s at least 12 months after your retirement. When you receive this payment, you’ll also be responsible for paying federal income taxes, Medicare taxes, and Social Security taxes.

You can elect to defer payments from this fund or annuitize it. To have this option available, you must request it at least 12 months before the first payment. That means you need to decide on deferring or annuitizing these funds during your last quarter of work at Chevron.

If you elect to defer or annuitize the RRP, the minimum deferral is five years; that means you’d receive your first payment six years after retirement. You can elect to receive from one to 10 installment payments, and any payments are made in January.

How Does Your Retirement Date Factor Into These Calculations?

The biggest impact can be related to determining your tax burden. If you’ve reviewed the benefits you expect to receive during your first year(s) of retirement and see you’ll be receiving multiple, high-value streams of income, it may make sense to defer your RRP to maximize tax efficiency.

Whenever you choose to retire, it’s important to fully consider the funds available to you from various retirement sources. Balancing and maximizing the benefits of each income source is important.

You shouldn’t select your retirement date in a bubble or base it on sentimental reasons like retiring on your exact hire date or finishing your career at the end of a calendar year. Instead, it makes sense to work with a financial partner to carefully choose your retirement date and select the option that gives you the greatest financial benefit.

At Willis Johnson & Associates, we have experience supporting hundreds of clients through the retirement process, and we’re very familiar with the various options available to Chevron employees. To learn more about how we can guide and support you through this planning process, review what we offer Chevron executives or dive into the many resources we’ve prepared especially for Chevron professionals.