When viewing your Fidelity NetBenefits online, you may see some additional accounts outside your BP 401(k) and your RAP pension:

- ECP – Excess Compensation Plan listed together with your ESP 401(k)

- The non-Qualified Pension ECP – Illustrated with your RAP Pension benefit

- EBP – Excess Benefit Plan listed together with your ESP 401(k)

These are non-qualified plans related to your BP retirement accounts, requiring some significant planning.

How Do BP's Non-Qualified Plans Work?

The ECP and EBP are "non-qualified" plans. Unlike the "qualified" 401(k) and "qualified" pension, these non-qualified accounts do not have the same protections in many ways. For example, they are subject to the creditor liabilities and financial health of BP, and they do not have the same personal creditor protections for the account owners. Also, the election options for these plans are much less flexible than the elections available in the 401(k) and pension plans.

BP's Excess Compensation Plan (ECP)

The ECP (for both the ESP and the RAP) is funded when your compensation – base and bonus (not any stock compensation) exceeds an IRS-specified dollar amount. Almost every year, these dollar amounts increase. In 2025, the dollar limit at which the ECP's funding begins is $350,000.

Impact of BP Pension and 401(k) Limits

When your base and bonus compensation reaches the limit, BP can no longer contribute their matching 401(k) contribution to your ESP account. Also, BP can no longer contribute their crediting amount for your RAP Pension to your pension's cash balance account. However, these contributions do not cease; BP pours these contributions over to the appropriate ECP accounts related to either the 401(k) or the pension.

Let's illustrate using an example. In 2025, Susana has a base salary of $320,000 and a target bonus of 25%. So, assuming no performance adjustment in her bonus, her compensation is $400,000 for 2025. When Susana receives her paycheck at the end of July, she will cross the $350,000 compensation threshold. As a result, BP will begin contributing its 7% ESP matching contribution to the ECP instead. Additionally, BP will contribute the company's crediting amount (a percentage based on Susana's age and years of service) to the non-qualified Pension ECP instead of her pension's cash balance account.

BP's Excess Benefit Plan (EBP)

The EBP, related only to the ESP 401(k), is funded when your contributions to the 401(k) over-fund the account and push BP's matching contribution out of the 401(k). How does that happen?

Certain limits pertain to 401(k) accounts for individual contributions and overarching contributions. First, there is the limit that you can contribute pre-tax or Roth, which is $23,500 ($31,000 for those 50 and over) in 2025. Then, there is the overarching limit for all contributions to your 401(k) account by you and BP. In 2025, the total 401(k) limit is $70,000, or $77,500 for those 50 and older. If you contribute enough such that your contribution and BP's contribution exceed these total limits ($70,000 or $77,500), BP's contribution will pour over to the EBP.

Let's continue with our example from earlier. In 2025, Susana (age 48) elects to frontload her ESP 401(k). Her goal is to have her bonus primarily fund her 401(k) and to have 401(k) funding completed earlier in the year so she can benefit from compounded growth. In the first quarter, Susana contributes the following towards her ESP 401(k):

- $23,500 in the Pre-Tax source

- $36,500 in the After-Tax source

As a super-saver, $60,000 seems deserving of a pat on the back for retirement contributions; however, Susana made a common mistake we see from high-earners at BP. By overcontributing to the pre-tax and after-tax sources within her 401(k), she has pushed out a significant amount of BP's 7% matching contribution to her ESP! Instead of the $24,500 BP can contribute on her behalf, she maxed out the 401(k) with only $10,000 in contributions from BP. And, Susana can't stop her contributions once she maxes out her pre-tax and after-tax source. She needs to push them to the EBP or she doesn't get the matching contributions from BP since BP's contributions are only via a match.

However, all is not lost for Susana. Upon reaching the $70,000 limit for 401(k) contributions, BP directs the remaining $14,500 of their 7% contributions to the EBP.

.png?width=600&height=338&name=BP%20-%20Non-Qualified_Retirement_Plans_at_BP_Blog_Graphic_Q4%202024%20(4).png)

Financial Planning Considerations for BP Professionals with the ECP or EBP

Monitor Contributions to the BP ESP

Avoid the EBP Pour-Over during Working Years

It should be noted from the above examples that the ECP pour-over is compulsory for those with compensation exceeding the limits. Therefore, there is no way to avoid the pour-over of BP's match if your compensation is too high.

However, you can mitigate the pour-over to the EBP with prudently crafted contribution strategies and monitored contributions throughout the year. Using a carefully calculated formula, you can make contribution elections for the pre-tax, Roth, and after-tax sources in the 401(k).

Review our guide to maximizing your BP savings here >>

You should monitor your pre-tax, Roth, and after-tax pools throughout the year. Many BP employees don't realize that contributions do not cease once you max out your pre-tax Roth limit of either $23,500 or $31,000, depending on your age. Instead, the contributions roll over to your non-Roth after-tax pool.

As you contribute more to the after-tax source, you increase the possibility that your contributions will push BP's match into the EBP. Therefore, you should monitor your total contributions for the year. When the employee and employer contributions hit the max limit - $70,000 or $77,500 for those 50 and over – the employer's ESP contribution pours over to the EBP.

Manage Investments in the ECP & EBP

Invest For Growth Now and Safety Later

The ECP and EBP have the same investments available in the ESP. The default investment is a target-date fund tied to your age and prospective retirement date. The Pension ECP does not have any investment choices as it is credited with interest based on your hire date with BP.

If you have an ECP for the 401k, you will have an ECP for the pension. Because the ECP for the pension receives regular interest credits and is not exposed to market volatility, you can view it as a conservative, fixed-income investment. You may want to be more aggressive with the investments in your 401(k) ECP and EBP. The default target-date funds will get progressively more conservative over time.

For example, you may wish to choose more of the stock funds in the available investment choices – the S&P Index.

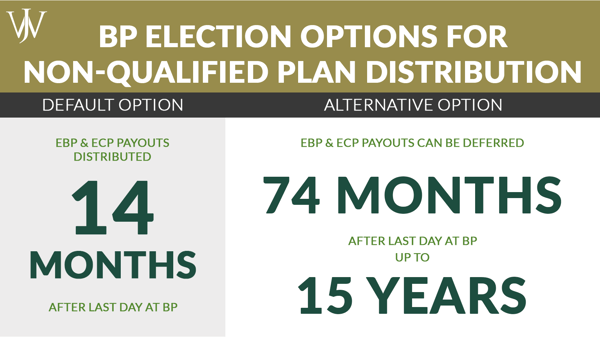

When you get closer to leaving BP, you will want to invest more conservatively in the 401(k) ECP and EBP accounts. Consider if the stock market should drop significantly before collecting your ECP and EBP benefits. Unless you choose any other election (as detailed below), these accounts will pay out 14 months after leaving the company.

Plan Elections For Income & Tax Planning Purposes

The default distribution for the non-qualified plans – the ECP and EBP related to the 401(k) - is 14 months after you leave BP.

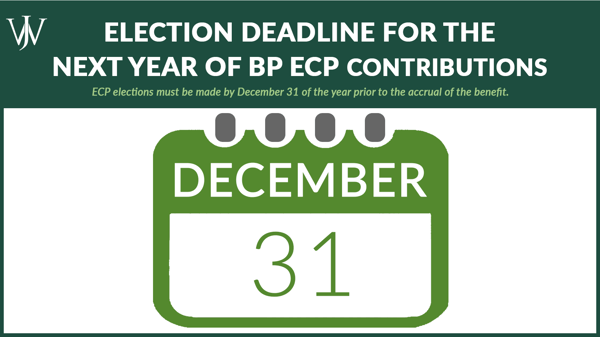

Advance Distribution Elections

Before accruing these benefits, you can make an election to accelerate or defer the payout of the benefit. You must make such an election by December 31 of the year before the accrual of the benefit. For instance, if you know your compensation is likely to exceed the compensation limits in 2026 and you are likely to accrue a benefit under the ECP savings plan, you could make an election to accelerate or defer the payout by December 31, 2025.

The advance distribution election for the Pension ECP is not available. The default distribution for the ECP related to the pension is also 14 months following your departure from BP.

If you choose to change the default or previously elected timing of the distributions from your ECP, EBP or Pension ECP, you can under the following parameters:

You must submit your distribution election no less than 12 months before the distribution date.

- Your election applies to all your non-qualified plans (except specific pre-2005 non-qualified plans).

- You can elect to receive a lump sum payment or a monthly, quarterly, or annual payment stream.

- Your election must be pushed out a minimum of five years (74 months after you leave the company) and can be pushed out up to 15 years.

What Non-Qualified Plan Elections Work Best?

It depends on a variety of situations and matters pertinent to you. The key considerations are cash flow and taxes.

Let's consider an example of prioritizing a BP retiree's cash flow. Chris is retiring from BP at age 54. Chris is mostly sure that he has enough non-retirement funds to last until age 59 1/2, when he can take penalty-free distributions from his retirement accounts. Still, he would like a bit more of a buffer. To ensure he has enough funds available at retirement, his most beneficial election is to distribute his non-qualified accounts 14 months past his retirement date.

Let's tweak our example slightly for a BP retiree prioritizing the tax impact instead. Suppose Chris leaves BP to take another highly compensated position at another company. Chris is concerned that his non-qualified plans will drive him well into the top tax brackets when added to his salary and bonus at the new company. Therefore, Chris opts to push out his distributions for 74 months so he will receive these payouts after his expected retirement when his income is lower.

Pay Attention & Have a Financial Strategy

The difficulty with non-qualified plans is twofold: to maximize the benefit, you have to know the plans well enough to develop a strategy and be disciplined enough to execute that strategy. To make the most of both the ECP and EBP, you must:

- Correctly allocate your contributions to the 401(k)

- Properly manage your investment allocation

- Be on top of your distribution elections

Partner with a Financial Advisor to Manage Your ECP & EBP Effectively

Managing your ECP and EBP properly requires continued maintenance and monitoring. Willis Johnson & Associates works with BP professionals to help them plan their future, develop contribution and allocation plans, monitor progress throughout the year, and implement the best distribution strategy to capitalize on the impact of these accounts. These non-qualified plans are complex. We help make them simple. Learn more about our process and client experience here.