As the end of the year approaches, it’s time to start making your list and checking it twice when it comes to your financial planning. BP professionals have a number of opportunities to save money and reduce their tax bill before year-end, and the time to take advantage of these opportunities is now.

Want to jump ahead to a specific item we discuss with our BP clients each year? Click the links below:

- Maxing out the BP 401(k)

- Contributing to the HSA

- Making charitable donations

- Reduce taxes through tax loss harvesting

- Review Open Enrollment elections & your estate plan

1) Max Out Your 401(k), the Employee Savings Plan (ESP)

Contributing to your 401(k) is one of the easiest ways to save for retirement. BP offers a generous company match, making this a priority checklist item to maximize your benefits.

BP’s 401(k) Match

BP employees are eligible for up to a 7% match, which means BP may contribute up to a total of $24,500 in 2025 of money you don’t want to miss out on. While you can contribute more than 4% of your pay (up to designated contribution limits), employees should ensure they are at least contributing 4% to receive the full BP matching.

401(k) Contribution Limits for 2025

Each year, the Internal Revenue Service (IRS) identifies contribution limits for 401(k) plans. The amount you contribute to your Employee Savings Plan in the pre-tax source reduces your taxable income dollar for dollar, however, any contributions made to Roth or After-Tax don’t reduce your taxable income. In 2025, if you are under 50 you may contribute up to $23,500 into the pre-tax or Roth sources of your 401(k). If you are over 50, this limit increases to $31,000 across the sources after catch-up contributions.

Across all sources, the total contribution limits to a 401(k) for 2025 are as follows:

- If You are Under 50: $70,000

- If You are Over 50: $77,500

These numbers change every year so re-evaluating your contributions annually is crucial to maxing out the ESP each year.

In addition to pre-tax, Roth, and the BP company match, there’s another source in the 401(k) called the after-tax source that employees can contribute to. The after-tax source isn’t as tax-efficient as pre-tax or Roth, but it provides a unique opportunity for what we call the Mega Backdoor Roth strategy which can be incredibly tax-efficient over time.

What’s the Mega Backdoor Roth Strategy?

The Mega Backdoor Roth strategy, also known as an After-Tax rollover, is a process that allows you to transfer after-tax contributions out of the 401(k) to a Roth IRA where your contributions can grow tax-free for life. Unlike pre-tax contributions, your after-tax contributions do not get deducted from your taxable income. However, converting the contributions to a Roth IRA every year to avoid taxable growth in the 401(k) can keep them growing without a tax drag, and when you take out qualified distributions during retirement, you get to take the funds tax-free. However, this strategy is not as simple as it seems. There can be significant tax implications if the process is done incorrectly or if there are any earnings in the after-tax account, so working with an advisor who has experience in this area is crucial.

Non-Qualified Plans & the BP 401(K)

The ESP is a unique plan that comes with great opportunities for long-term planning (as we see with the Mega Backdoor Roth strategy) and for simply made mistakes. In 2025, if you’ve properly maxed out your employee contributions and received the maximum company match from BP, you can put up to $22,000 into your after-tax source within the 401(k). However, we often see employees over-contribute to the ESP, which pushes BP’s company match contributions over to a non-qualified plan called the Excess Benefit Plan. This non-qualified plan isn’t as tax-efficient at retirement when it pays out compared to the 401(k). Often, we try to help our BP clients avoid this pour-over by closely monitoring ongoing ESP contributions instead.

Perform a Self-Audit to See If You’re On Track to Max Out Your BP ESP This Year

Many BP professionals believe that they have maxed out their Employee Savings Plan by making the most of their pre-tax contributions. However, we perform a simple audit with clients that you can use to ensure you’ve maxed out the 401(k) each year in both the pre-tax and after-tax sources.

To see if you’ve maxed out the ESP, use the following steps to pull up your contribution summary.

1. Log in to your Fidelity NetBenefits account2. Select Your BP Employee Savings Plan 401(k) account

.png?width=600&height=250&name=EOY_Blog_2024_12_600x25_Graphics%203%20(4).png)

3. Under the “Summary” tab, select “Statements” .png?width=672&height=84&name=image%20(23).png)

4. Choose Year to Date to see this year’s data (or use the specific date feature to look at previous years), and click “Retrieve Statement”

.png?width=403&height=133&name=image%20(22).png)

5. Scroll down to “Your Contribution Summary” and review your contributions -1.png?width=470&height=237&name=Untitled%20design%20(1)-1.png)

Often, we see many BP professionals’ contribution summaries look something like this if they believe they’ve maxed out the 401(k) for their age and their income meets the IRS 415 income limitations in a given year.

You may look at this and think, “They’ve saved over $50,000, so surely this person is at the maximum in the 401(k), right?”

Unfortunately, this individual left their after-tax pool empty, which means they’ve missed an opportunity to add $10,500 to their retirement savings!

How Income Limits Impact 401(k) Contributions in 2025

If you’ve already accumulated over $350,000 in income in 2025 between base and bonus, and your goal is to max out the 401(k), your summary should read as follows:

- Employee After-Tax: $22,000

- Company Contribution: $24,500

- Employee Pre-Tax (if over age 50): $31,000

So, what should you do if you notice this error in the future?

If you’ve left money on the table, you can adjust your contributions for 2025 to allocate funds to the after-tax pool. However, if it looks like you will not make the maximum contributions this year, you can increase your contribution percentage over your final pay periods as a final push to increase your savings. Although, if your base and bonus have pushed you over the $350,000 income limit threshold for this year, you will have to wait until 2026 to begin making 401(k) contributions again.

When making your elections for 401(k) contributions in 2025, the proper formulas for maxing out the Employee Savings Plan are as follows:

If you make under $350,000 in base & bonus:

(After-Tax or Pre-Tax/Roth Limit Based on Your Age) / Salary = Percentage Allocation

If your base & bonus exceeds $350,000:

(After-Tax or Pre-Tax/Roth Limit Based on Your Age) / $350,000 = Percentage Allocation

When the compensation limits for 2026 are released, using the formulas above with the new limits can be an effective way to maximize your Employee Savings Plan contributions throughout the year.

Using the formula for someone over age 50 making $350,000 in base and bonus compensation in 2025, below is an example of what the contributions should look like in the employee pre-tax and employee after-tax contribution sources each month to be considered on track to max out.

|

|

Compensation Accumulation |

Bonus |

Cumulative Employee Contributions to After-Tax |

Cumulative Employee Contributions to Pre-Tax |

|

End-of-Year Targets |

$255,000 |

$95,000 |

$22,000 |

$31,000 |

|

January |

$21,250 | - | $1,381.25 | $2,125 |

|

February |

$42,500 | - | $2,762.50 | $4,250 |

|

March |

$158,750 | $95,000.00 | $10,318.75 | $15,875 |

|

April |

$180,000 | $11,700.00 | $18,000 | |

|

May |

$201,250 | $13,081.25 | $2,012.50 | |

|

June |

$222,500 | $14,462.50 | $22,250.00 | |

|

July |

$243,750 | $15,843.75 | $24,750.00 | |

|

August |

$265,000 | $17,225.00 | $26,500.00 | |

|

September |

$286,250 | $18,606.25 | $28,625.00 | |

|

October |

$307,500 | $19,987.50 | $30,750.00 | |

|

November |

$328,750 | $21,368.75 | $31,000.00 | |

|

December |

$350,000 | $22,000 | $31,000.00 | |

|

Total Compensation |

$350,000 |

Total Contributions |

$22,000 |

$31,000 |

In this example, the calculation required a 10% contribution each month to pre-tax and a 6.5% contribution to after-tax. With these contribution elections, the employee maxes out both sources by the end of the year.

We frequently discuss this process with our clients when determining strategies to employ to make the most of their 401(k) contribution elections.

If you’d like to learn more or realize you've left 401(k) contributions on the table, reach out to us to set up a complimentary conversation with one of our fiduciary advisors.

2) Contribute to Your Health Savings Account

Another simple action BP employees can leverage to minimize their taxable income is making contributions to HSA or FSA accounts. FSAs operate on a “use it or lose it” principle, so it’s important to use the funds by December 31st! For HSAs, the contribution deadline for 2025 is April 15, 2026. After December 31st, contributions won’t come from the 2025 payroll, but can still be made out of pocket and deducted on your tax return. Health savings accounts (HSAs) offer triple tax benefits, providing a great way to save for medical expenses. The catch is that HSAs are only available to high-deductible medical plan participants.

In 2025, you can put up to $8,550 into a family HSA or $4,300 for an individual account if you’re under age 55. If you’re over 55, there’s an additional $1,000 catch-up allowed for each type of account. Much like pre-tax contributions, HSA contributions reduce your taxable income dollar for dollar!

Additionally, BP contributes $1,000 to employees' HSA accounts if they meet certain criteria. And, if your spouse works at BP as well, they’ll contribute $2,000 of free, tax-advantaged dollars which can yield significant savings over time!

Flexible Spending Account (FSA)

For those with flexible spending accounts, December 31st is crucial for a different reason. With an FSA, the funds operate on a “use it or lose it” basis. Before year-end, you must use any of the funds you’ve placed in the account for qualified expenses, or you’ll lose access to the funds. If you’re nearing the end of the year and don’t have any major medical expenses left to cover, you can also spend the funds on medical products included on sites such as FSA Store.

3) Make a Charitable Donation

Another way to trim your tax bill is to give to charities. Charitable contributions can be deducted from your taxable income, and in some cases, BP may offer a matching gift program. Make sure to check with HR to confirm eligibility.

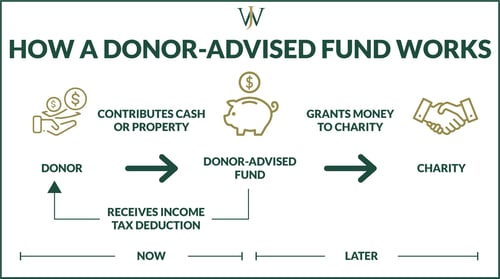

Donor-Advised Funds (DAFs)

One way that you can do this is to set up a donor-advised fund, making regular and irrevocable contributions. Donor-advised fund contributions allow for multi-year contributions to be made in one year, with the benefit of immediate tax deductions in the year the gifts were made to the DAF. Once inside the DAF, the assets are allowed to grow and given to charity over whatever time you deem appropriate. This strategy can be an effective way to avoid paying capital gains taxes, helping you keep thousands of dollars in your accounts.

When we talk about charitable gifts, remember that they can be made in cash or stock. The transfer of cash is quick and easy. However, it can be more beneficial to gift appreciated stock into your DAF to avoid taxes on the gains. Gifting your appreciated stock allows you to not only get a deduction of the amount transferred but also avoid paying capital gains on the appreciated stock.

4) Reduce Your Taxes Through Tax-Loss Harvesting

At WJA, one of the things we pay special attention to for our clients is taxes and lowering their tax burden over time. Using the tax-loss harvesting strategy, we sell positions in our client’s portfolios at a loss to offset potential capital gains and minimize their taxes for a given year. The IRS allows taxpayers to apply an offset of up to $3,000 to reduce their taxable income each year.

Something we at WJA do, especially in down markets, is sell positions at a loss to offset potential capital gains. Any losses not offset by gains can be applied to reduce taxable income up to $3,000. Any additional losses may be carried over into the following years until they are used. Learn more about this strategy here >>

5) Review Your Open Enrollment Options & Your Estate Plan

Because BP’s Open Enrollment is early in the new year, the end of the year is the perfect time to make sure your life & disability insurance coverage is adequate to protect your family in the event of your death.

In addition to AD&D provided by BP, you can purchase additional coverage as well as contribute to a cash accumulation account that works similarly to your 401(k) contributions. This provides another vehicle for before-tax savings.

Don’t forget to review your current financial needs against your disability insurance coverage elections as well. While disability premiums are not a direct savings vehicle, it’s important to regularly reassess your coverage as finances change throughout your life.

Finally, review your estate planning documents including your last will and testament and your designated power of attorney. You might also include a living will and a medical power of attorney in case you become mentally or physically handicapped before your death. Everyone should have an estate plan regardless of age, wealth, or social status. Creating trusts or detailing directives for asset transfers can be part of a long-term tax strategy that helps keep generational wealth in your family. Download our Estate Planning Checklist here >>

Optimize Your Financial Future with End-of-Year Tax Planning

For many, the later months of the year are filled with celebration and anticipation for the new year. However, it’s also a time ripe with the opportunity to manage taxes and set yourself on a strong financial foundation for the years ahead. By taking advantage of these opportunities, you may be able to save money, reduce your tax bill, and support your financial future. At WJA, we proactively work with our BP clients to take advantage of the unique financial planning opportunities available to them as the year comes to an end so they can leverage them effectively. If you’re curious about what opportunities are available to you, reach out to our team for a complimentary discussion and discover what you can do to make the most of the season.