The IRS has recently released the 2026 retirement plan contribution limits, and starting January 1, 2026, many provisions under SECURE Act 2.0 are officially underway. For super-savers at Shell, this is great news. Shell employees can now contribute $24,500 (or $32,500 for those over 50 years old) of pre-tax or Roth savings to the Shell Provident Fund and can get up to $88,250 (or $98,350 for married couples aged 55-60) of retirement savings into tax-efficient vessels including the HSA, in 2026.

| Source | Under 50 | Age 50-55 | 55-59, 64+ | 60-63 |

|

Fully maxing out all 401(k) sources

|

$72,000

|

$80,000

|

$80,000

|

$83,250

|

| Backdoor Roth |

$7,500

|

$8,600

|

$8,600

|

$8,600

|

|

HSA (family, +1 catch up where applicable)

|

$8,750

|

$8,750

|

$9,750

|

$9,750

|

| Total Retirement Savings | $88,250 |

$97,350

|

$98,350

|

$101,600

|

How Much Is Shell's 401(k) Contribution?

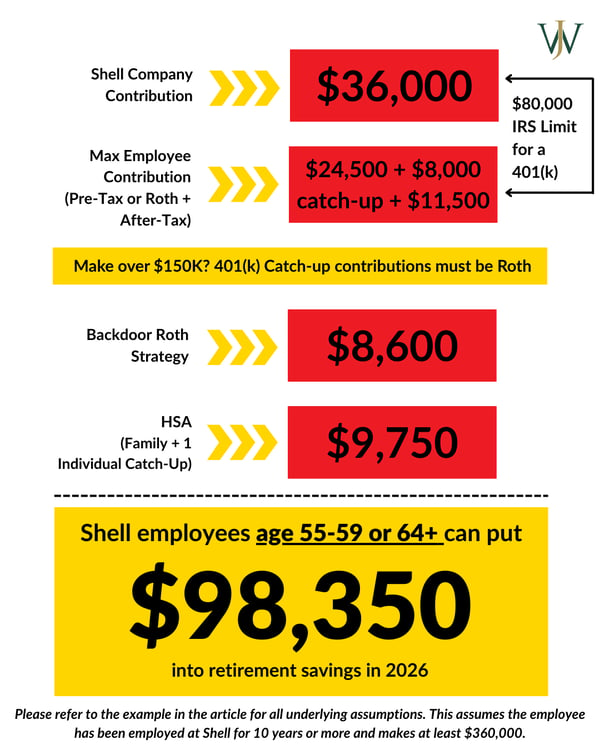

Shell offers a 10% contribution to 401(k) accounts for employees who have been with the company for over nine years. Since the annual 401(k) income limit for 2026 is now $360,000, Shell will cap company contributions to the Provident Fund at $36,000.

How Shell Employees Can Max Out the Shell 401(k) if Under Age 50

If you’re under age 50, the total IRS limit for 401(k) contributions in 2026 from employee or employer contributions is $72,000. Here's how it breaks out:

- In Pre-tax or Roth: Employees under age 50 can contribute up to $24,500 across the two sources

- In Non-Roth After-Tax Contributions: The maximum Shell allows for after-tax contributions is $11,500 in 2026.

- Shell's Employee Contribution: Shell contributes anywhere from 2-10% of an employee's compensation to their 401(k) each year. The maximum Shell can contribute in 2026 is $36,000 due to the IRS' income limits.

.png?width=600&height=750&name=Shell%20-%20Max%20Savings_Shell_Blog_2024_Q4_2025%20Contribution%20Limits_Under%2050%20(4).png)

How to Max Out Your Shell 401(k) in 2026 If You're Age 50 or Older

If you’re over age 50 and under age 60, the total IRS limit for 401(k) contributions in 2026 from employee or employer contributions is $80,000, broken out as follows:

- In Pre-tax or Roth: Employees in these age brackets can contribute up to $32,500 across the two sources, thanks to a $8,000 catch-up allowance.

Following the passage of SECURE Act 2.0, starting in 2026, catch-up contributions must be designated as Roth contributions for individuals making over $150,000 in annual income. This income threshold is indexed annually for inflation. - In Non-Roth After-Tax Contributions: The maximum Shell allows for after-tax contributions is $11,500 in 2026.

- Shell's Employee Contribution: The maximum amount Shell will contribute to an employee's Provident Fund in 2026 is $36,000 due to the IRS' income limits.

.png?width=601&height=751&name=Shell%20-%20Max%20Savings_Shell_Blog_2024_Q4_2025%20Contribution%20Limits_Age%2050-54%20(9).png)

In addition to the 401(k), there are valuable savings opportunities in vehicles such as the Backdoor Roth or HSA (which has additional catch-ups once you reach age 55). If you’re maxing out all of these sources alongside the backdoor Roth and full HSA contribution limit for families with an individual catch-up, you could save $98,350 in tax-efficient vehicles in 2026!

Super Catch-Up Contributions at Age 60-63 Starting in 2026

Employees aged 60 to 63 after January 1, 2026, can contribute even more to workplace retirement plans thanks to legislation under Secure Act 2.0. Individuals in this age group have a higher catch-up contribution amount, indexed each year for inflation.

With the passage of SECURE Act 2.0, individuals age 60-63 can contribute over and above standard and catch-up limits to their 401(k)s for retirement.

.png?width=600&height=750&name=Shell%20-%20Max%20Savings_Shell_Blog_2026%20Contribution%20Limits_Age%2060-63%20(1).png)

In addition to the standard catch-up contribution, individuals age 60-63 can contribute the greater of $10,000 or 50% more than the standard catch-up limit. Because the standard catch-up contribution limit for 2026 is $8,000, the maximum catch-up contribution allowed for individuals age 60-63 is $11,250 for 2026.

Sounds exciting, right? To get this right, you need to be mindful of a few important caveats. For high-income earners (your income exceeds $150,000 for the year), these catch-up contributions must be made as Roth contributions and are not tax-deductible. Second, not all employer plans support these contribution limit amounts, so confirm with HR or your 401(k) Summary Plan Descriptions before making your 401(k) elections for the year.

For super-savers at Shell, this change provides a valuable opportunity for older employees to enhance their retirement savings as they approach retirement. Employees in this 4-year age bracket maxing out their Shell Provident Fund, a family HSA with catch-ups, and backdoor Roths can save up to $101,600 in 2026!

.png?width=600&height=750&name=Shell%20-%20Max%20Savings_Shell_Blog_2026%20Contribution%20Limits_Age%2060-63%20(2).png)

Smart Savings Strategies After Maxing Out Your 401(k): Backdoor Roths, HSAs, and More

Roth accounts are one of the most effective ways to grow wealth for the future because your money grows tax-free. Contributions are made with after-tax dollars, so when you retire, you can withdraw both your contributions and earnings without owing taxes. For many Shell professionals, this helps create flexibility in retirement by balancing taxable and tax-free income and keeping more of what they’ve worked hard to earn.

Backdoor Roth

The IRA contribution limit for 2026 increased to $7,500 ($8,600 if age 50+). Though many high-income earners are prevented from directly contributing to a Roth IRA, many Shell employees can take advantage of the backdoor Roth strategy to get more saved in Roths each year. This strategy is nuanced and can cause more harm than good if enacted poorly, so be sure to discuss it with a financial advisor if you want to incorporate it into your financial plan.

Shell Employees Can Save on Taxes Using a Mega Backdoor Roth with After-Tax 401(K) Contributions

Additionally, if you are contributing after-tax dollars to the Shell Provident Fund, you can roll out the after-tax funds annually to a Roth IRA to take advantage of the mega backdoor Roth strategy for additional tax savings over time.

How to Use Shell's HSA (Health Savings Account) for Tax-Optimized Savings

A Health Savings Account (HSA) is often an under-utilized benefit that provides a unique triple tax advantage for those looking to save more each year:

- Tax-Deductible Contributions: Contributions made to an HSA are tax-deductible, which means they lower your taxable income in the year you make the contribution. This can reduce your overall tax liability.

This year, Shell employees can contribute up to $8,750 (or $9,750 if they are over age 55 and both spouses are taking advantage of the catch-up contribution) for a family. For individuals, the maximum HSA contribution is $4,400. - Tax-Free Growth: The funds in your HSA can be invested, and any earnings or capital gains from these investments are tax-free as long as they remain in the account. This allows your savings to grow over time without incurring taxes.

- Tax-Free Withdrawals for Qualified Medical Expenses: The withdrawals are entirely tax-free when you use the HSA funds for qualified medical expenses.

When using an HSA as a retirement fund, Shell employees can benefit from both tax deductions and tax-free growth, making HSAs a valuable tool for long-term savings and retirement planning.

High earners should consider using both plans strategically – what do savings amounts look like if you max out the 401(k), leverage the backdoor Roth, AND max out your HSA this year in each situation?

| Source | Under 50 | Age 50-55 | 55-59, 64+ | 60-63 |

|

Fully maxing out all 401(k) sources

|

$72,000

|

$80,000

|

$80,000

|

$83,250

|

| Backdoor Roth |

$7,500

|

$8,600

|

$8,600

|

$8,600

|

|

HSA (family, +1 catch up where applicable)

|

$8,750

|

$8,750

|

$9,750

|

$9,750

|

| Total Retirement Savings | $88,250 |

$97,350

|

$98,350

|

$101,600

|

What If You Make Over the 401(k) Compensation Limit in 2026?

The annual compensation limit for 2026 has increased from $350,000 to $360,000. If you make over $360,000 in base and bonus compensation for 2026, remember to max out your Provident Fund contributions before reaching that income threshold. After you earn $360,000 of income, both you and Shell can no longer contribute to the Provident Fund.

What Happens if You Make More than the 401(K) Income Limits?

In 2026, once you earn more than $360,000, Shell will contribute to the Shell Provident Fund BRP (Benefit Restoration Plan) instead of the Shell Provident Fund. If 2026 is the first year you expect to make over $360,000, check that you have an allocation and investment strategy for your Provident Fund BRP.

The 2026 limit adjustments will be advantageous for super-savers at Shell, and it is crucial to be sure that you make the most of these changes.

Get a Tailored Savings Plan From an Advisor with Specialized Shell Benefits Knowledge

At Willis Johnson & Associates, we work with our Shell clients to help them get the full 10% company contribution, take advantage of backdoor Roth IRAs, and facilitate after-tax roll-outs from the Provident Fund to help optimize retirement savings. If you have any questions about the 2026 contribution and compensation limits, please contact your advisor or schedule a free consultation with one of our Shell specialists.